For All Subscribers

This release includes changes required by the One Big Beautiful Bill Act (“OBBBA”), which had many tax provisions.

The following are the provisions implemented in Family Law Software.

Family Law Software will perform all the related calculations automatically, unless otherwise noted below.

1. 2017 Tax Act changes are made permanent. The 2017 tax act made a number of changes in prior law, including the following:

- Lowering tax rates and brackets.

- Substantially increasing the standard deduction.

- Setting the personal exemption amount to $0.

- Reducing deductibility of mortgage interest.

- Limiting the deductibility of state and local taxes.

- Increasing the child tax credit.

- Introducing the Qualified Business Income (QBI) deduction.

- Eliminating miscellaneous itemized deductions.

- Reducing applicability of the Alternative Minimum Tax.

- Making alimony non-taxable and non-deductible.

- For the Child Tax Credit, the start of the phase-out is increased to an AGI of $200,000 ($400,000 in the case of a joint return).

Except for this last item, these were all scheduled to sunset (revert to pre-act rules) at the end of 2025. OBBBA makes them all permanent, except as noted below.

2. Standard deduction. The standard deduction in 2025 is set at $31,500 for joint filers, $23,625 for head of household, and $15,750 for all other filers. It will be increased for inflation.

3. Senior deduction. There is a new Senior Deduction of $6,000 per year for each party over age 65 at year-end.

- This deduction is available to parties regardless of whether they itemize their deductions.

- It does not apply to parties who are married filing separately.

- The deduction is reduced by 6% percent of adjusted gross income minus $75,000 ($150,000 in the case of a joint return).

- It will be entirely phased out at AGI of $175,000 ($250,000 on a joint return where one party is over age 65, and $350,000 in the case of a joint return where both parties are over age 65).

- The deduction applies only to tax years 2025 through 2028.

Family Law Software looks at the birth date of each party. It will automatically apply the senior deduction if the party is over age 65 at year end.

4. Child tax credit. In addition to making the 2017 changes permanent, the act permanently increases the nonrefundable child tax credit to $2,200 per child beginning in tax year 2025.

- It also permanently indexes the nonrefundable credit amount for inflation beginning after tax year 2025 (rounded down to the nearest $100).

- The $1,700 refundable amount will also be adjusted for inflation.

Family Law Software will handle these changes automatically.

5. Qualified Business Income Deduction (QBID). The act made a couple of changes to the QBID.

- There is a new minimum Qualified Business Income Deduction QBID of $400 (as adjusted for inflation from 2025 rounded to the nearest $5) when a party has at least $1,000 (as adjusted for inflation from 2025 rounded to the nearest $5) of qualifying business income.

- The taxable income limitation phase-in now starts at $75,000 ($150,000 for a joint return).

- When filing jointly, the parties’ QBIDs are added together.

- These changes take effect in 2026, not 2025.

6. Alternative Minimum Tax (AMT). The act makes a couple of changes to the AMT.

- The phase-out percentage will be 50%, starting in 2026.

- As noted above, the act permanently extends the increased individual Alternative Minimum Tax exemption amounts.

- The act also reverts the exemption phaseout thresholds to 2018 levels of $500,000 ($1,000,000 in the case of a joint return), indexed for inflation thereafter.

The latter two changes will work in opposite directions: the increased exemption amounts tends to reduce AMT; the reverted phaseout thresholds tends to increase AMT. But the upshot is that, under the act, very few individuals will be subject to the AMT.

7. Home mortgage interest. The act makes changes to retain the reduced deductibility of home mortgage interest.

- As noted above, the act permanently lowers the deduction for qualified residence interest to the first $750,000 in home mortgage acquisition debt.

- Also, interest on home equity indebtedness continues not to be deductible.

- However, the act allows certain mortgage insurance premiums on acquisition indebtedness to be counted as mortgage interest, starting in 2026.

In Family Law Software, we have decided not to implement the deduction for mortgage insurance premiums at this time, as it will not have a significant impact on taxes and adds complexity. The software will take care of the other changes automatically.

8. Reduction of itemized deductions. Not for 2025, but effective in 2026, there is a new reduction of itemized deductions.

- It is now calculated as: (2/37) * the smaller of a) itemized deductions; and b) (taxable income before itemized deductions minus the the 37% tax bracket amount).

- One exception: taxable income for QBI is to be computed without this limitation.

Family Law Software automatically calculates the deduction and subtracts that from itemized deductions, to get the allowable amount of itemized deductions.

9. SALT cap. The act temporarily increases the cap on permitted itemized deductions for state and local taxes (SALT) to $40,000 for 2025.

- This cap increases by 1% per year from that level through 2029.

- The cap then reverts to a flat $10,000 ($5,000 if married filing separately) in 2030 and beyond.

- Prior to 2030, the cap is subject to a phaseout for taxpayers with incomes above $500,000 ($250,000 if married filing separately).

- The phaseout causes the cap to be reduced by 30% of (Modified AGI – (500,000*(1.01^(CurrentYear-2025)))). (In this expression, “CurrentYear” means the year, e.g., 2026, 2027, etc., and “^” means “raised to the power of.”)

- But the phaseout may not reduce the deduction below $10,000 (or $5,000 if married filing separately), so that is the lowest the allowable SALT deduction will go.

Family Law Software calculates these phase outs automatically..

10. Deduction for tips. Up to $25,000 of qualified tip income is deductible for individuals in traditionally and customarily tipped industries for tax years 2025 through 2028. Treasury has released a list of those industries.

- This deduction is available regardless of whether the parties itemize their deductions.

- There is no deduction if you are married filing separately.

- There are also information-reporting requirements from employees to employers, and from employers to the IRS.

- There are other qualifications as well (which will not limit the deduction for most people).

- The deduction is phased out by 10% of each dollar of modified AGI that exceeds $150,000 ($300,000 if filing jointly).

- It is fully phased out at a modified AGI of $400,000 ($550,000 if filing jointly).

- In practice, the phase-out is not likely to apply to most tipped individuals.

Family Law Software calculates this deduction automatically. It treats all tips as qualifying. If tips are earned that are not qualifying, you should enter them on a different line.

11. Deduction for overtime. Up to $12,500 ($25,000 if filing jointly) of qualified overtime income is deductible for individuals in for tax years 2025 through 2028.

- This deduction is available regardless of whether the parties itemize their deductions.

- After 2028, there is no overtime deduction.

- There is no deduction if you are married filing separately.

- There are also information reporting requirements by employees to employers and by employers to the IRS.

- There are other qualifications as well (which will not limit the deduction for most people).

- The deduction is phased out by 10% of each dollar of modified AGI that exceeds $150,000 ($300,000 if filing jointly).

- It is fully phased out at an AGI of $275,000 ($550,000 if filing jointly).

Family Law Software calculates this deduction automatically. It treats all overtime income as qualifying. If overtime is earned that is not qualifying, you should enter it on a different line.

12. Interest on vehicle loans. Some interest on vehicle loans is deductible in 2025 through 2028. The qualifications are:

- It must be a new automobile or motorcycle

- It must be purchased in 2025 through 2028.

- It must have had final assembly in the United States.

- Only the first $10,000 in interest is deductible.

If the rate were 5%, that would mean that a loan of up to $200,000 would fully qualify. More limitations:

- The deduction is reduced by 20% of the amount by which modified AGI exceeds $100,000 ($200,000 if filing jointly).

- It is fully phased out for modified AGI of $150,000 ($250,000 if filing jointly).

This will typically mean that anyone with an Adjusted Gross Income over $150,000 will not be eligible for this deduction. So unlike the income phase-outs on many other tax law provisions, the income phase-out on this one may significantly limit the deduction for many people.

This deduction is available regardless of whether the parties itemize their deductions.

In Family Law Software, here is how you indicate that the interest on the loan qualifies:

- Enter the loan as a debt.

- Click the more info button.

- Scroll down and check the box to indicate that this is a vehicle whose interest qualifies for the deduction.

Family Law Software will automatically calculate the interest on the loan(s), add up all qualifying loans, calculate the phase-out, and limit the deduction to the years 2025 through 2028.

13. Child Care Credit. After 2025, the child care credit rules change.

- This provision increases the maximum credit rate to 50 percent (currently 35 percent).

- It is reduced by one percentage point, but not below 35 percent, for each $2,000 or fraction thereof by which the taxpayer’s AGI exceeds $15,000.

- It is further reduced (but not below 20 percent) by 1 percentage point for each $2,000 ($4,000 in the case of a joint return) or fraction thereof by which the taxpayer’s adjusted gross income for the taxable year exceeds $75,000 ($150,000 in the case of a joint return).

Some examples for a single individual (single or head of household filing status):

- If income is $15,000, the credit percentage is 50%, and the credit can be as much as $3,000.

- In 2025, these are 35% and $2,100.

- In 2025, these are 35% and $2,100.

- If income is $35,000, the credit percentage is 40%, and the credit can be as much as $2,400.

- In 2025, these are 25% and $1,500.

- In 2025, these are 25% and $1,500.

- If income is $85,000, the credit percentage is 30%, and the credit can be as much as $1,800.

- In 2025, these are 20% and $1,200.

In Family Law Software, there is nothing you need to do. The software will reflect these changes automatically.

14. Charitable contributions for non-itemizers. Starting in 2026, non-itemizers can claim a deduction of $1000 ($2000 if filing jointly) for charitable donations.

In Family Law Software, if a party is claiming the standard deduction, and they have made charitable contributions, we calculate a charitable contribution deduction for their charitable donations in an amount up to the limit.

There is nothing you need to do. The software will reflect these changes automatically, starting in 2026.

15. Charitable contribution reduction for itemizers. Starting in 2026, the itemized contribution for charitable contributions is reduced by 0.5% of AGI. For example, if AGI is $100,000 and charitable contributions are $2,000, the deductible amount is $2,000 – (0.5% of $100,000), or $1,500.

Family Law Software will do this adjustment automatically. Note that there are other limitations on charitable contributions, and Family Law Software is not tracking those limitations.

16. Trump Accounts. The bill creates a new kind of IRA called Trump Accounts.

- Contributions are not tax-deductible.

- The account belongs to a child.

- A US citizen born in the years 2025-2028 for whom a Trump Account is established will receive an initial $1,000 deposit from the government.

- Parents and others may contribute up to $5,000 annually, adjusted for inflation. This amount is reduced by any employer contributions.

- Employers may contribute up to $2,500 per year per child, adjusted for inflation, not taxable to the recipient or their family.

- Deposits in Trump Accounts must be invested in low-cost stock market index funds.

- Deposits cannot be withdrawn prior to the beneficiary turning 18 years old.

- After that point, the account generally is treated as a traditional IRA (Individual Retirement Account) and generally is subject to the same withdrawal rules as other traditional IRAs.

- Trump Accounts may be created during or after 2026, but not before.

If a Trump Account is set up, enter it in Family Law Software as a Roth IRA and specify that it is a child’s account. That will capture the non-deductible nature of the contributions and allow for employer contributions. Distributions from Trump Accounts will be taxable, and distributions from Roth IRAs are not taxable. so we are not exactly capturing all of the characteristics of these accounts. Distributions are not likely to occur for many years, however, so, for now, we are adequately capturing the provision.

Aside from the tax act, here are the changes in this release.

1. On Income and Expense screen, we clarified whose expenses are being viewed. Here is the new header:

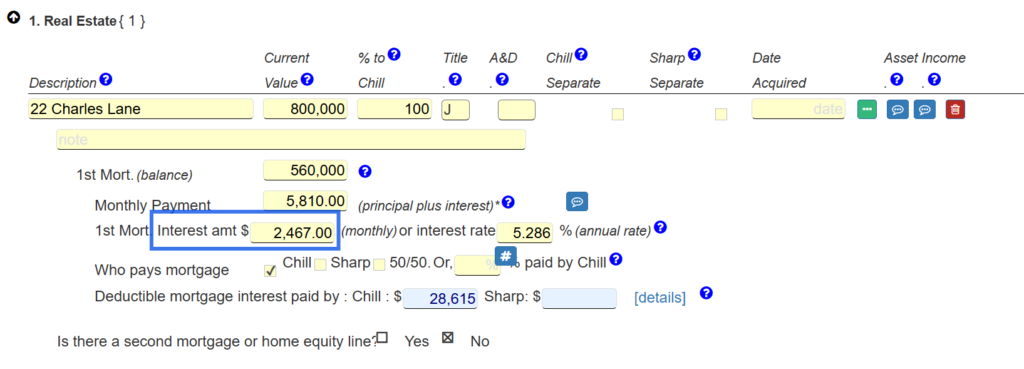

2. For mortgages, it is now possible to enter an interest amount, instead of an interest rate. So if you know the amount of interest paid in a month, but not the interest rate, you can enter the amount instead. You can see this in the image below.

State Specific

California

- Updated forms FL-142 and FL-142S.

- Updated Judicial council forms 313-INFO, C, K, and V.

- Updated Judicial Council Forms 314-INFO, C, K, and V

- Updated Judicial Council Forms 320-INFO, S

Florida

- Updated Arrears rate.

- Updated minimum wage rate.

New Jersey

- Corrected footer codes for Sole and Shared guideline worksheets.

- Updated Appendix IX-H

- Updated Certification of Non-Military Service.

- Updated Summary Affidavit