There are a number of tax breaks for parents, which we have covered in an earlier blog post.

This blog post zeroes in on the strategy of alternating who claims the child as an exemption.

Before the 2017 tax changes, claiming a child as an exemption meant (1) an extra personal exemption and (2) a Child Tax Credit for the child on the parent’s tax return.

The 2017 tax changes suspended the federal personal exemption, at least until 2026, so claiming a child as a dependent directly affects only the Child Tax Credit (and any state tax benefits). However, the Child Tax Credit is worth as much as $2,000 in federal tax savings per year per child, so it very much merits the parties’ attention.

Who Can Claim the Exemption?

Unlike tax breaks such as Head of Household filing status and the child care credit, which depend on where the child lives most of the time, the exemption for children is negotiable between the parties in a divorce.

The majority-time parent typically claims the child as a dependent, but the parties can agree between them that the other parent will claim the child instead. (In that case, the majority-time parent has to to give the other parent a signed IRS Form 8332 allowing the other parent to claim the child. The parent claiming the child will file Form 8332 with their federal return.)

Who Should Claim the Exemption?

With the help of a divorce or tax professional, the parties can determine who will benefit the most from claiming the child. They can agree that that party will claim the child, regardless of the custody arrangement, and compensate the other party.

However, it’s not always possible to know who will benefit the most, let alone quantify the benefit, from claiming the child in future years.

Also, sometimes parties care less about the actual net financial benefit, and more about the appearance of fairness in the claim of exemptions.

In either event, one popular approach is for the parties to alternate the years in which each will claim the child. One party claims in the current year. The other party claims in the following year. And so on, alternating the claim of exemption each year. (When there is an even number of children, the parties can also agree to have each party claim half the children each year.)

Implementing Alternating Exemptions

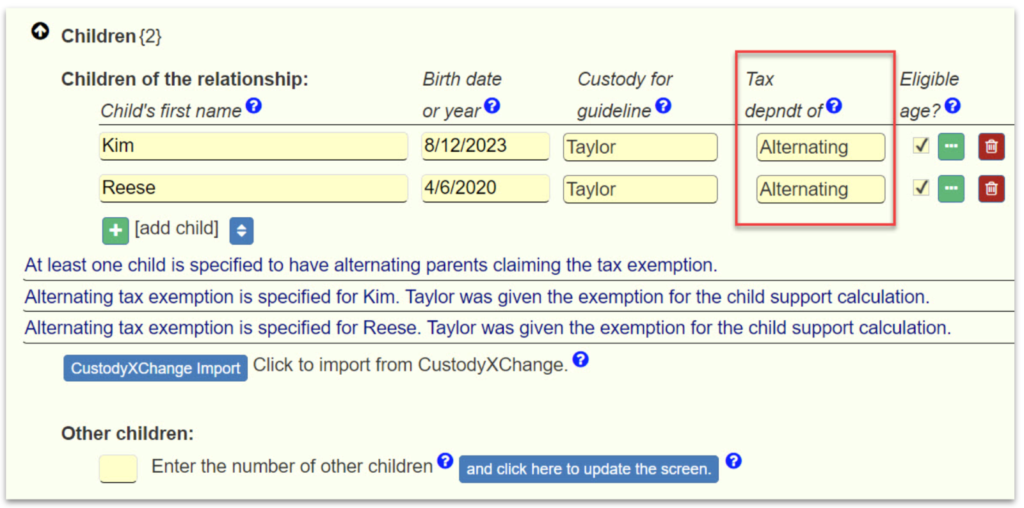

To implement the alternating exemptions strategy in Family Law Software, choose “Alternating” where the program asks who will claim the child:

The program assumes that the first party will claim the child in year 1, the other party will claim the child in year 2, and so on. To change who goes first, click the “more info” box (green with three dots in the screen image) and explicitly specify which parent will go first.

Impact on Child Support

One side-effect of claiming the exemption in alternating years is that it can cause the calculation of child support to alternate each year as well.

This will happen in states where federal and/or state taxes are deductions in the calculation of guideline net income for child support purposes. What happens is the following:

- The exemption reduces a party’s tax.

- That lower tax increases the after-tax income available to that party.

- That higher income increases that party’s child support amount.

This means that the child support amount would bounce back and forth each year between two values, depending on who claims the exemption each year.

Dealing With The Impact

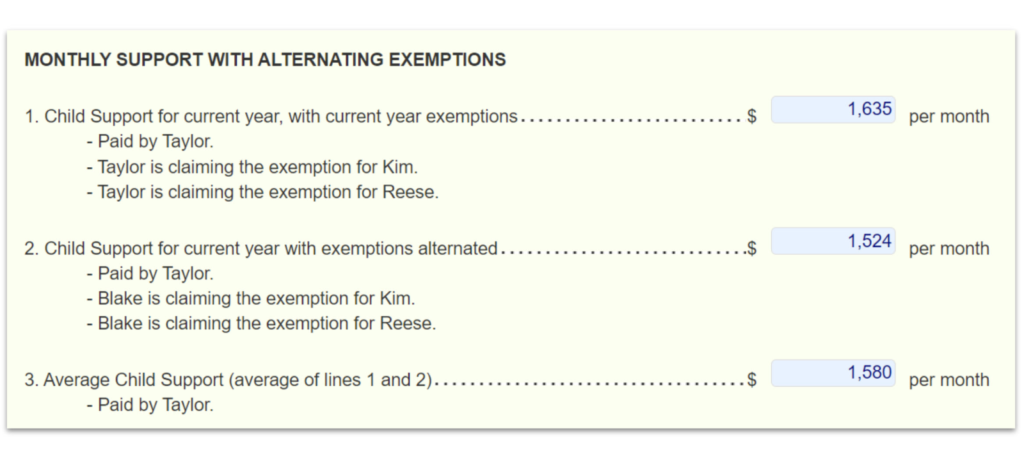

How can the parties deal with that up front? One way is to agree on a child support amount that is the average of the two child support amounts.

Family Law Software calculates the official amount using the current-year exemption, as the statute requires. But it also appends a worksheet to the child support guideline for the use of the parties and the court. The appended worksheet shows:

- Child support payer and amount in year 1.

- Child support payer and amount with the exemption switched.

- The average of the child support amounts in 1 and 2.

If the parties and the court agree, this average can then be used for the child support order.

This enables the parties to alternate exemptions and have the child support order reflect the anticipated tax impact of the switch.