Trial and Order

We can give you a receipt if you pay for a full year, but we are not set up to send receipts for the regular monthly billing.

The charge on your credit card statement will serve as your receipt.

Yes, we have a Macintosh version of the software.

It runs natively — no need for Parallels or other Windows emulation.

You may open on your Macintosh files you created on Windows, and vice versa.

And you may upload and download between the Mac version and the Cloud.

We do offer the option of charging monthly, and you may cancel your subscription at any time, but we do not support “suspending”a subscription.

The reason for this is that it would not be viable for us, either economically or administratively, because many people would call us to suspend when they have a dry month, then call again to resume when they have a busy month.

The set-up fee is $99, which is 1-2 months’ subscription charges.

If you know that you will not be using the software for more than two months, you may cancel, and then resume later and pay the one-tine charge again.

We do not encourage this, as we will incur the administrative costs of suspending and resuming the subscriptions if you do that.

But we do allow it.

We thank you for your understanding in this regard.

For the most up-to-date information about products and pricing, please click here.

The following notes address the most commonly-asked questions:

- The Basic Edition does not include any of the analytical or reporting tools. Most of our subscribers have the Cloud or Firm edition.

- If you are a solo practitioner with no staff, we recommend the Cloud Edition.

- If there are multiple individuals in your office, including any staff, who will be using the software, we recommend the Firm Edition.

- There is no risk to signing up because all products come with a 60-day money-back guarantee.

- All products also include the option for a desktop version. Files may be uploaded and downloaded between the Cloud and desktop software.

- We do not import the files of any other software. To transition, wrap up existing cases in the old software and start new cases in Family Law Software.

- For a list of getting-started resources, please click here.

If you have not had enough time to evaluate the software during the free trial, we invite you to send us an email at support@familylawsoftware.com, requesting us to extend the trial.

Family Law Software is both easier and more powerful. Specifically:

- Family Law Software is easier to learn and easier to use.

- Family Law Software has all the key entries for Florida Child Support on a single screen.

- Family Law Software makes it very easy to see the results of the alternative methods with split custody.

- Family Law Software is more stable (very rarely crashes).

- In particular, customers have told us that Family Law Software handles mortgages much better.

- Family Law Software’s Florida Financial Affidavit looks better.

- Family Law Software has a worksheet for modifications and also generates the Income Deduction Order (IDO) and Income Withholding Order (IWO).

- Family Law Software generates both the official child support guideline form and the DPA guideline form.

- Especially with high income families, Family Law Software’s tax calculation is more accurate, because we automatically include the alternative minimum tax.

- Family Law Software desktop installs via download and is easy to install on multiple computers (no charge for paralegals or administrative assistants).

- Family Law Software desktop runs on both Windows and Macintosh.

You will see customer comments, some of which compare Family Law Software to DPA here:

Customer Comments

In our experience, virtually every DPA subscriber who has tried Family Law Software has switched to Family Law Software.

You may see for yourself, by downloading a free trial copy of Family Law Software here.

Download free trial

Family Law Software is a much more complete solution for the Family Law practitioner. Specifically:

- Family Law Software’s property division is completely integrated and easy to use. No export/import needed.

- On the Case Information Statement (CIS), Family Law Software allows you to print footnotes with each line item from within the software — no need to print to a word processor first to add footnotes.

- Family Law Software performs detailed tax calculations for the current year. This allows you to give accurate budget estimates for all clients.

- Family Law Software contains an easy-to-use calculation of the amount of spousal support needed to cover a recipient’s budget.

- Family Law Software contains an easy-to-use calculation of the amount of spousal support needed to reach a 50/50 division of cash after taxes.

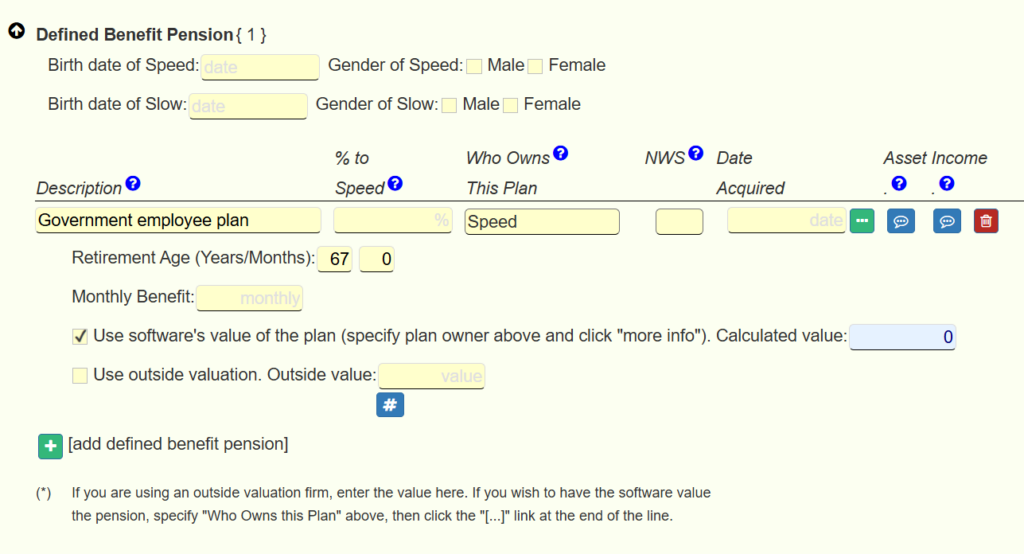

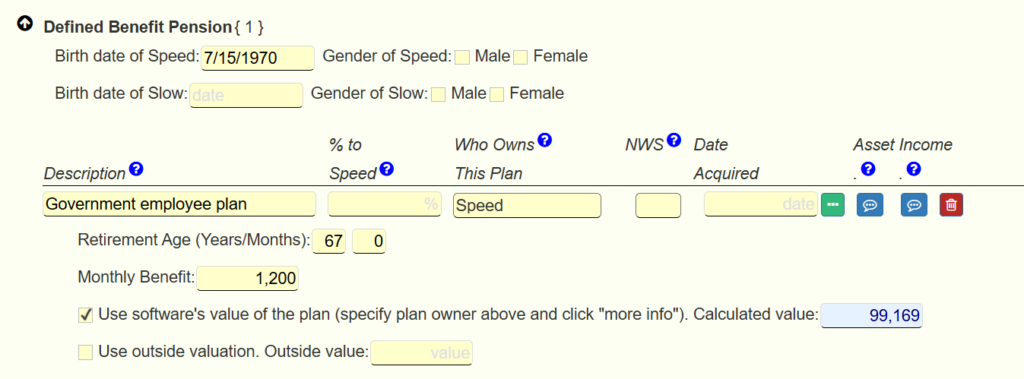

- Family Law Software generates a defined pension benefit valuation that is as actuarially accurate as any appraiser.

- Family Law Software allows you to do cash flow projections for up to 50 years in the future.

- Family Law Software has numerous charts and graphs for such things as Income after support and taxes, Alimony Needed, Who Should Claim Exemptions, Best Filing Status, and more.

- Family Law Software runs locally, so it is very fast, but data files can be stored in DropBox, Google Drive, Microsoft OneDrive, or any other cloud folder system that integrates with Windows and Macintosh. So you get the best of both worlds: speed of operation plus accessibility of files from anywhere.

Family Law Software is also easier to learn and use. For example:

- Family Law Software has all the key entries for the Child Support calculation on a single screen.

- Family Law Software installs via download and is easy to install on multiple computers (no charge for paralegals or administrative assistants).

And one final bonus:

Family Law Software runs on both Windows and Macintosh!

You will see customer comments, some of which compare Family Law Software to EasySoft here:

New Jersey Customer Comments

You may download a free trial copy of Family Law Software here.

Download free trial

One big difference is that Family Law Software runs in your browser, which brings some important advantages:

- Run from any device.

- Don’t worry about where files are stored.

- Always current (we updated with enhancements regularly).

- Full-text search on pages.

- Make font sizes larger or smaller.

Substantively, Family Law Software is a much more complete solution for the Family Law practitioner. Specifically:

- Family Law Software has an equitable distribution worksheet that is completely integrated and easy to use.

- Family Law Software performs detailed tax calculations for the current year. This allows you to give accurate budget estimates for all clients.

- Family Law Software has numerous charts and graphs for such things as Income after support and taxes, Alimony Needed, Who Should Claim Exemptions, Best Filing Status, and more.

- Family Law Software contains an easy-to-use calculation of the amount of spousal support needed to cover a recipient’s budget.

- Family Law Software contains an easy-to-use calculation of the amount of spousal support needed to reach a 50/50 division of cash after taxes.

- Family Law Software generates a defined pension benefit valuation that is as actuarially accurate as any appraiser.

- Family Law Software allows you to do cash flow projections for up to 50 years in the future.

- Family Law Software runs locally, so it is very fast, but data files can be stored in DropBox, Google Drive, Microsoft OneDrive, or any other cloud folder system that integrates with Windows and Macintosh. So you get the best of both worlds: speed of operation plus accessibility of files from anywhere.

Family Law Software is also easier to learn and use. For example:

- Family Law Software has all the key entries for the Child Support calculation on a single screen.

- Family Law Software installs via download and is easy to install on multiple computers (no charge for paralegals or administrative assistants).

And one final bonus:

Family Law Software runs on both Windows and Macintosh!

You will see customer comments, some of which compare Family Law Software to SupportCalc here:

Pennsylvania Customer Comments

You may download a free trial copy of Family Law Software here.

Download free trial

This can happen in several situations.

Macintosh

If you are using the Macintosh edition, you do need a KeyCode for the trial version on the Desktop.

For all trial users, the KeyCode is “TRIAL” (in all capital letters).

Prior Users

If you have previously been a subscriber, you may download the trial edition for desktop only if you “start from scratch.”

To do that, uninstall the software from your computer and remove the Family Law Software folder.

To uninstall, in Windows, click the Windows “Start” Button and search for “Uninstall Family Law Software.”

To remove the Family Law Software folder, use Windows File Explorer, navigate to Documents, and drag the Family Law Software folder to the Recycle bin. Or, right-click on the Family Law Software folder and select “Delete.”

Other Situations

If you are trying the software for the first time, on Windows, and you get that message, please contact us and let us know. We will make sure you can get up and running.

If you are using the desktop software, check to see whether you have entered a KeyCode. This will be on the Files & Settings tab, at the top.

If you have not yet entered the KeyCode:

You need to enter your KeyCode into the software.

If you know your KeyCode, click Files & Settings > KeyCode/Account > New Keycode.

If you do not know your KeyCode, click Files & Settings > KeyCode/Account > New KeyCode > Download Keycode.

If that does not work, contact us to ask.

If you have already entered a KeyCode:

If you have already entered your KeyCode, try entering your KeyCode again, following the steps above.

If that does not work, contact us.

The IDFA free trial is a limited-time free trial to allow you to complete the IDFA training course.

Because this is downloaded software, we do not know when you start using it, or even if or when you download it.

Therefore, we start your trial period running on the date you receive the e-mail from us. (This is usually around the date you sign up for the IDFA course.)

The free trial is a special limited offer, and we are not able to grant extensions.

We offer a two-month full-money-back guarantee, so you may subscribe, then cancel and get a refund during that two-month period if you wish.

So if you want to use the software only to complete the course, you may do so, then cancel for a full refund (as long as it is within the two-month period).

Question: What are the key license terms?

Answer:

- The software is month-to-month and requires no contract.

- Tech support is free and included in the cost of the license.

- Software updates incur no additional charges.

Additional terms are specific to the edition:

Firm Edition

- Each attorney in the firm needs a license.

- All paralegals and staff receive free licenses.

Cloud Edition and Basic Edition

- The licensee may share their license with staff, but only one person may be logged in at a time.

Full Edition (Desktop)

- The software may be installed on multiple computers that are used by the licensee.

- Each professional that uses the software should have a license.

- Paralegals and assistants may use the software under an attorney’s license. They install on their computers and use the attorney’s name, email, and KeyCode.

Our ironclad subscriber guarantee: If dissatisfied for any reason, cancel within 2 months for a full refund. After that, your contract is month-to-month with no contract or obligation. You may cancel at any time.

The desktop software runs on Windows and Macintosh computers.

It is downloaded from the Internet and then runs locally on your computer.

The Windows software takes about 125 megabytes (MB) on disk.

The Macintosh software takes about 500 megabytes (MB) on disk.

No emulator is required for the Macintosh version. (You do not need VMWare or Parallels.)

The requirements of your computer are as follows:

Windows

The Windows version runs on Windows 11, Windows 10, Windows 8, Windows 7, or Vista.

Macintosh

The software runs on Macintosh operating systems including and after Macintosh OS X 10.13 (High Sierra, released in 2017).

Windows Server

The software does run successfully in a Windows Server environment.

Citrix

The software does run successfully in a Citrix environment.

The Cloud software runs in Chrome, Brave, and Firefox browsers.

We charge a set-up fee for two reasons.

1. Tech support. New subscribers tend to require more tech support, so this charge helps to cover that cost.

2. No contract. We have a “no contract” policy, which means that you may cancel at any time. This is a great benefit. However, some of our subscribers who pay monthly, who do not do much family law work, might be tempted to subscribe in January, cancel in February, subscribe in March, cancel in April, and so on. Administratively, we are not set up to be able to handle this kind of activity. And economically it would not be viable for us. So another reason for the one-time charge is to put a cost on this kind of switching.

We appreciate your understanding.

We really do hope you choose to subscribe.

And we would like to emphasize that if you do subscribe, we have a two-month full money-back-guarantee, a guarantee which covers the set-up fee as well.

So there is no risk in giving it a try. And if you don’t think it is well worthwhile, you have two full months in which to cancel for a full refund, again, including full refund of the set-up fee.

We get many requests to waive the set-up fee, for all kinds of reasons, many of them quite reasonable.

We have a set-up fee for two reasons.

First, we allow people to cancel at will. If people did not have a set-up fee, they would cancel when they did not have work, and resubscribe when they did. Administratively, that would be more than we can manage. Also, economically it would not be viable for us.

Second, technical support tends to be higher at the beginning of a subscription, and the set-up fee helps us compensate for that fact.

If we granted any waivers, that would not be fair to all the similarly-situated people who paid the fee.

Also, we would have to decide on a case-by-case basis whether to waive the set-up fee. This would represent an insupportable burden on our time.

Sometimes people intended to sign up at a conference where we were waiving the set-up fee, but did not quite decide in time.

If we waived the fee for those people, it would not be fair to the people who did take the plunge at the conference itself.

We allow people to cancel the software at any time. The caveat to that is that, when people re-subscribe, we charge the set-up fee again.

Again, if we waived the fee in that case, we would be incurring the costs described above, and it would be a slippery slope to the on-again off-again subscription arrangement that is not sustainable for us.

Our goal is to make the set-up fee be the smallest possible amount that would prevent the constant cancel-and-resubscribe, and that yields some return to cover the greater tech support costs.

We hope that this amount does not deter you from subscribing to our great software!

We strongly believe that even in one or two cases per year, the software more than pays for itself in the enhancement of the quality of work you do, the efficiency savings, increased profitability, and referrals from happier clients.

Getting Going

When you are starting the software, if you get the message saying “Family Law Software has encountered a problem and needs to close,” it is because a file did not download completely or has become corrupted.

Just download the software again, starting at the link below, and you should be fine.

Download Professional Edition

If this download seems to happen instantaneously (that is, in 3 seconds or less), then the software did not actually download again. You still have the faulty download.

This can happen because your browser is insisting that the software has already been downloaded, and so you could not have wanted to download it again.

In that case, if you restart your computer, that should clear your browser’s memory of having downloaded the software before, and this should enable you to download it again.

As you probably know, downloading is just the first step. In order to complete the installation, you need to run the download. You may be prompted to allow Family Law Software to make changes to the computer.

Click on it, then on our license agreement, Next, Next, and then Finish.

At that point, the software is installed and you should be good to go.

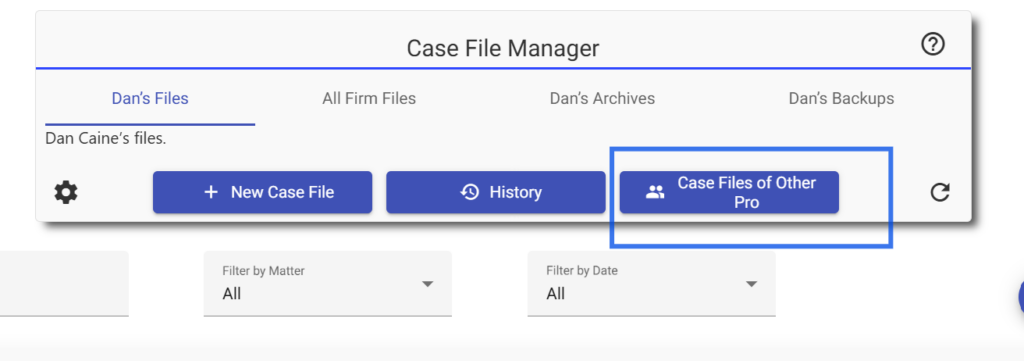

If you have the Firm Edition of the software, you can retrieve the files of a former attorney, or an an attorney or other professional who has left the firm.

Here’s how:

Log in to the software.

Open the File Manager (top right).

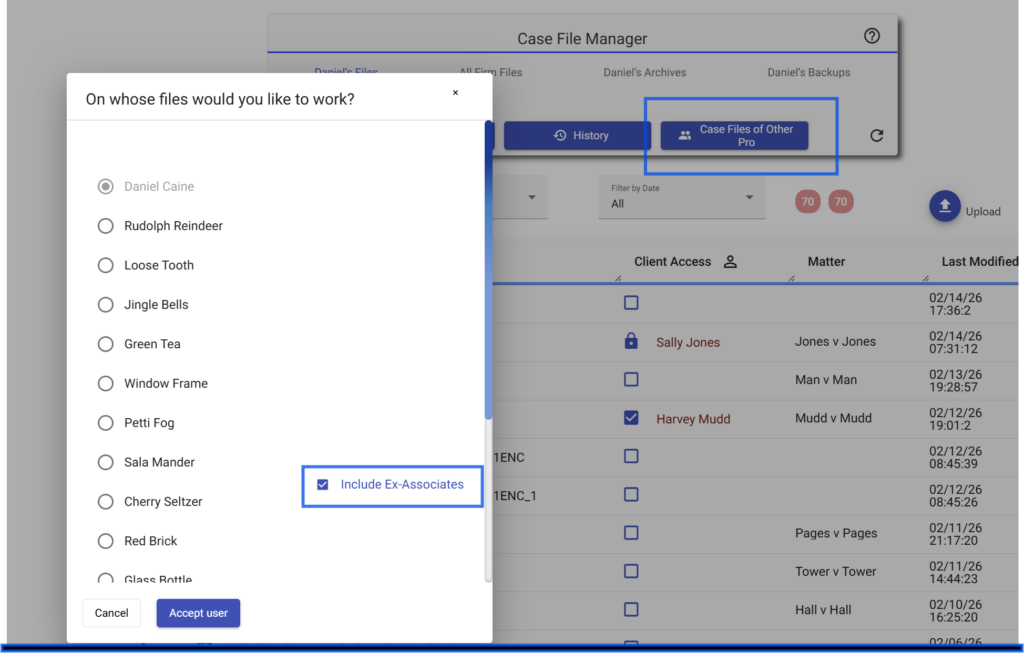

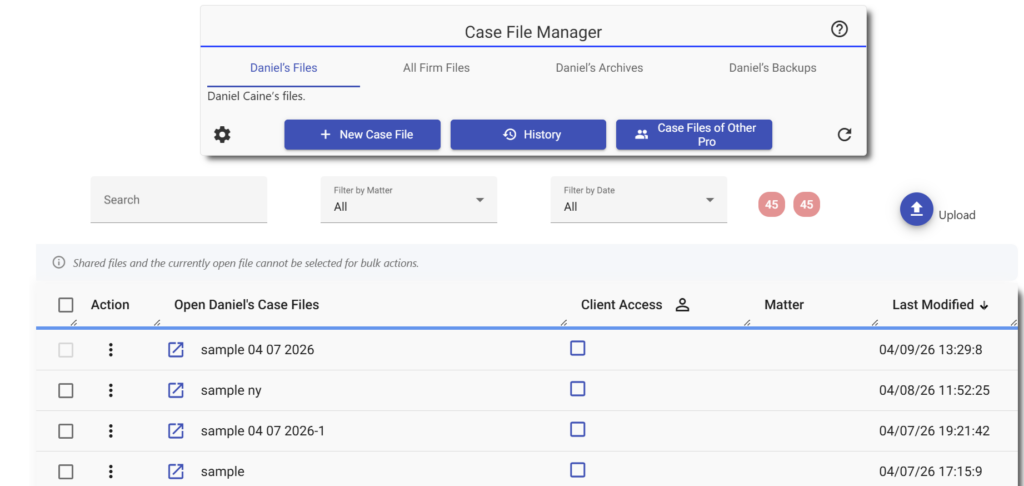

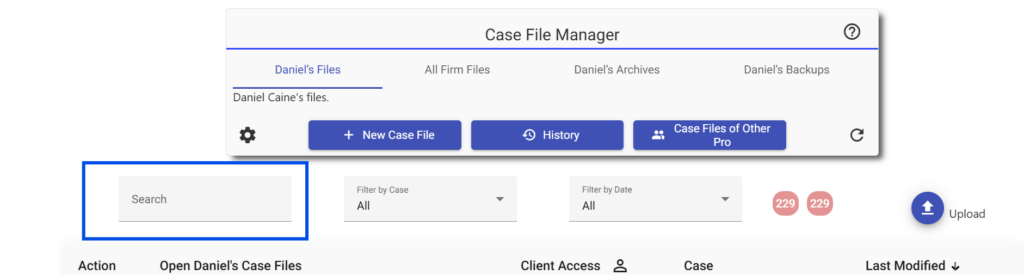

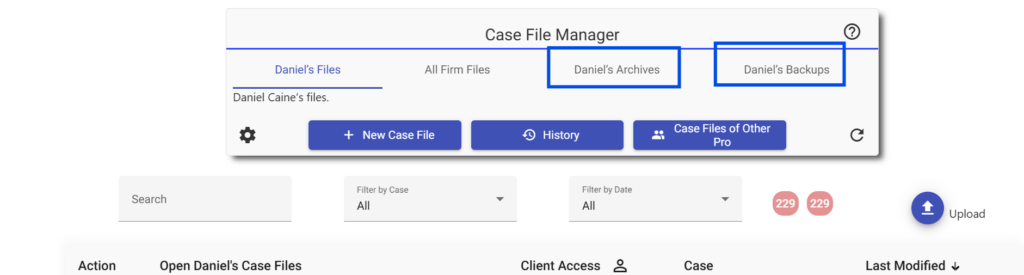

At the top of File Manager, click “Case Files of Other Pro” as shown below.

In the dialog that appears, click the checkbox to include files of ex-associates, as shown below.

The names of former associates will then be included in the list, and you will be able to open their files.

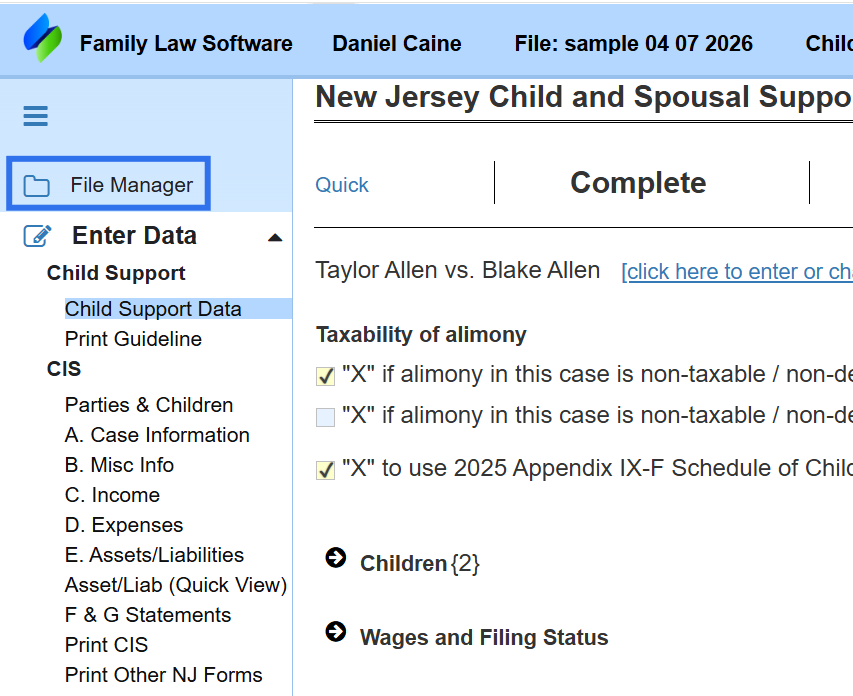

We are often asked whether we have updated the software for the latest changes, whether they be changes in the tax law, child support guideline updates, or revised financial forms.

Here’s how you can tell, if you are using the Cloud software (logging in at pro.flsgo.com):

- For child support guideline changes:

- Go to the screen where you enter child support.

- At the top of that screen, click the Complete link.

- At the top of the Complete screen, look for check boxes which specify which child support guideline you would like to use.

- If you see the latest one, then we have updated.

- If you see older ones, but you do not see the latest one, then we have not yet updated.

- If you do not see any checkboxes, then we do not support older guideline statutes in that state. In that case, search your email for an email from us, because we typically will send an email to all subscribers in a state when we update that state.

- Also search our version notes.

- For federal tax law changes:

- Please look for a blog post from us because we typically release a blog post when we update the software.

- Also, please check your email because we typically will send an email when we update the software.

- Search our version notes.

- For state tax law changes:

- Please check your email.

- Search our version notes.

If you are using the desktop software:

- Update your software to the latest release.

- Follow the steps described above for the Cloud software.

Google Chrome attempts to be “smart,” and not download a file that has already been downloaded.

Instead, it copies the file from a place it had already been saved (“cached’) on your computer. When it does that, you do not get the latest Family Law Software update.

Because it looks like it is downloading, it is hard to tell. (If it really is downloading, you can see the megabytes tick upward. If it is just copying a saved file, the download appears to be instant.)

In order to be sure that you are actually downloading from Family Law Software, you want to clear your browsing data.

Search the Internet for “how can I clear my browsing data for Chrome” (or fill in the name of your browser, such as FireFox, Edge, Safari, etc.)

After you have done that, return to the Family Law Software download page, and download the software again.

Click here to go to the Download page.

Simply click here and follow the instructions to download and install.

You may install this version right over your existing version.

As you probably know, downloading is just the first step.

In order to complete the installation, you need to run the download. You may be prompted to allow Family Law Software to make changes to the computer. Allow that.

In the Cloud, click Ctrl + (hold down the Ctrl key and click the “+” sign.)

On the desktop, click Files & Settings > Configuration >System Options > Use larger fonts for screen display.

Once you have checked this box and clicked OK, you have to exit the software and then start the program again.

This makes the fonts larger on-screen, but it does not affect the fonts that are used in printing.

The fonts will remain larger each time you use the program in the future, unless you return to this location and clear that checkbox.

There is no way to change the fonts that are used in printing.

This is because most of the outputs are carefully spaced with respect to the page, and we cannot increase the font size and retain the page layout.

In Windows, you can make all the fonts in the system larger. Open Settings and search on “fonts.”

This FAQ is for the situation where you are getting a new computer (PC or Macintosh) and want to install the software on it and move all of your files over.

It is also helpful if your computer has crashed, and you are moving to a new computer for that reason. (In that case, skip the parts that do not apply.)

Here are the steps to follow.

1. Back up existing client files.

The first step is to back up all of your client files.

If the files are already backed up on a network or in DropBox (or similar online storage), you can skip this step.

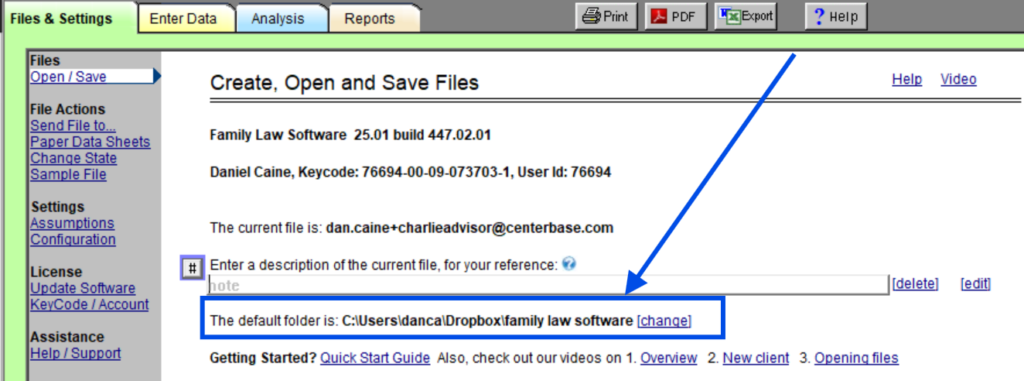

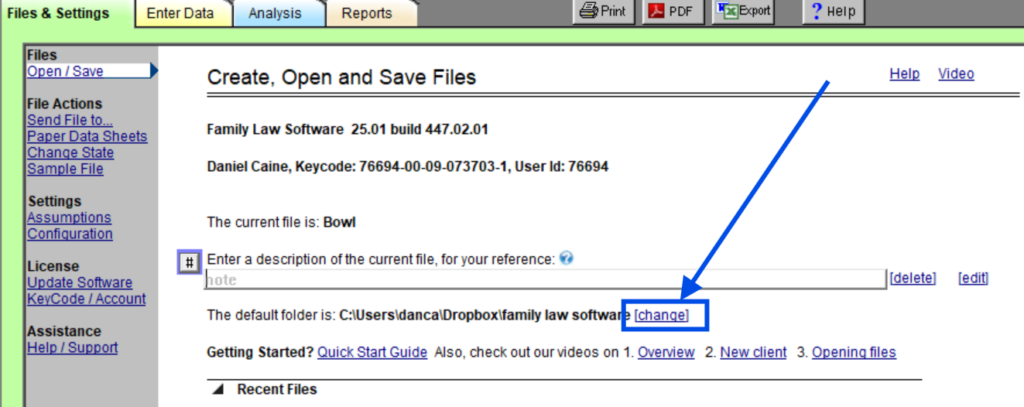

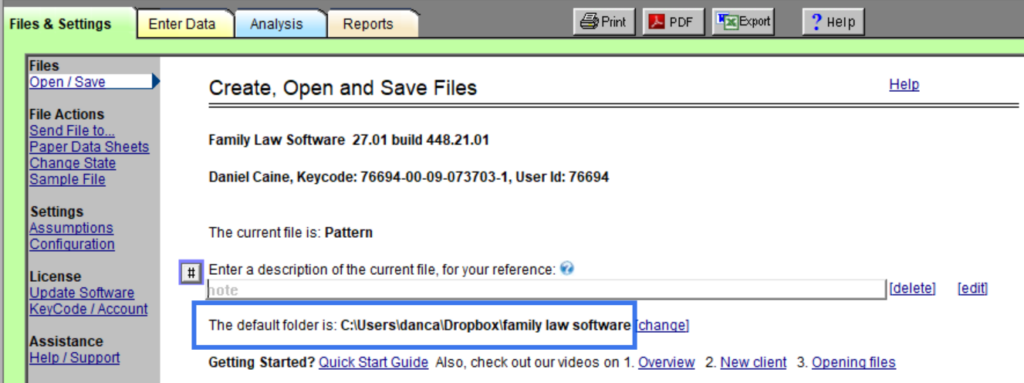

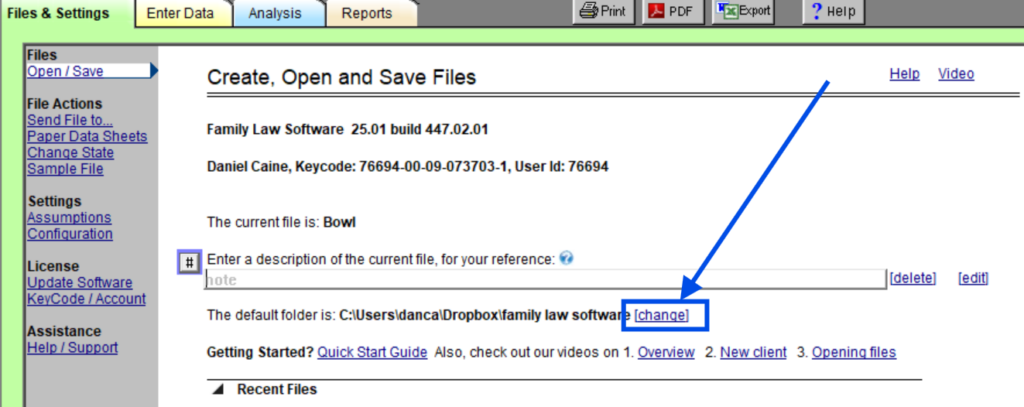

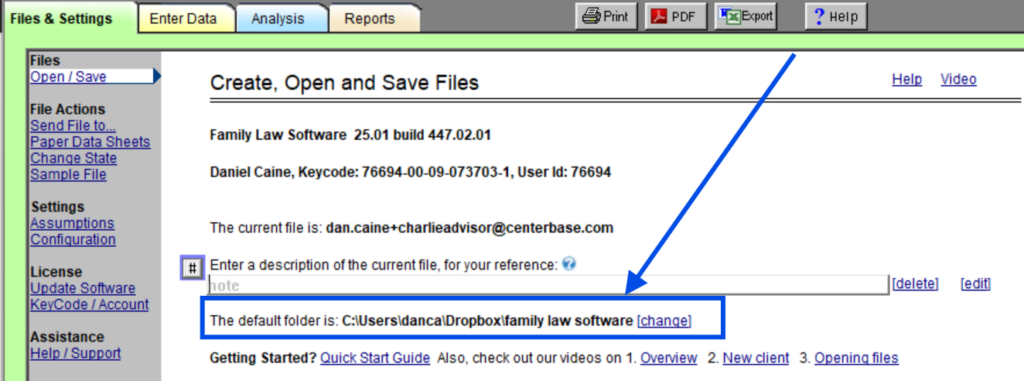

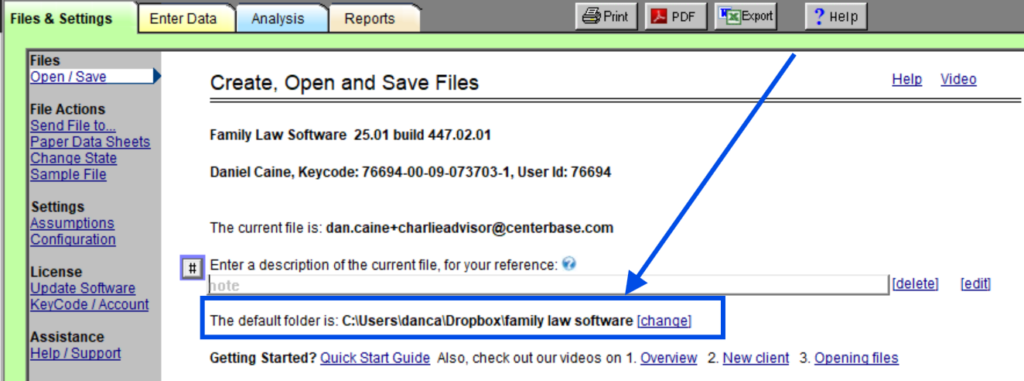

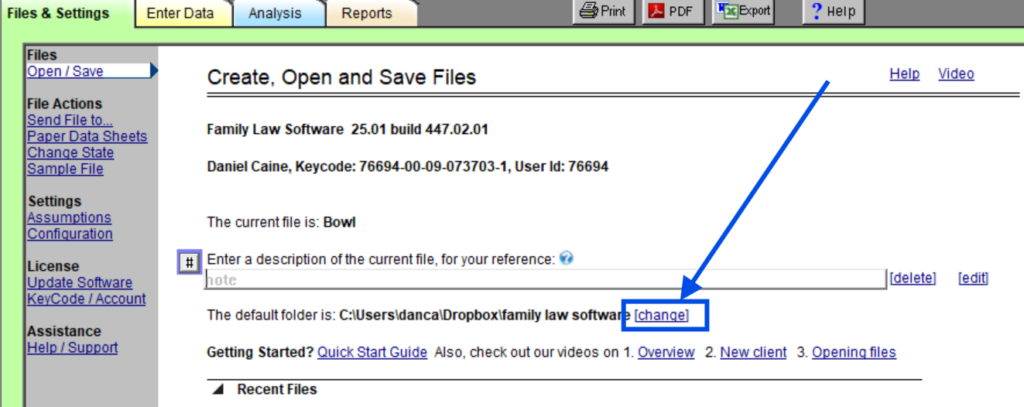

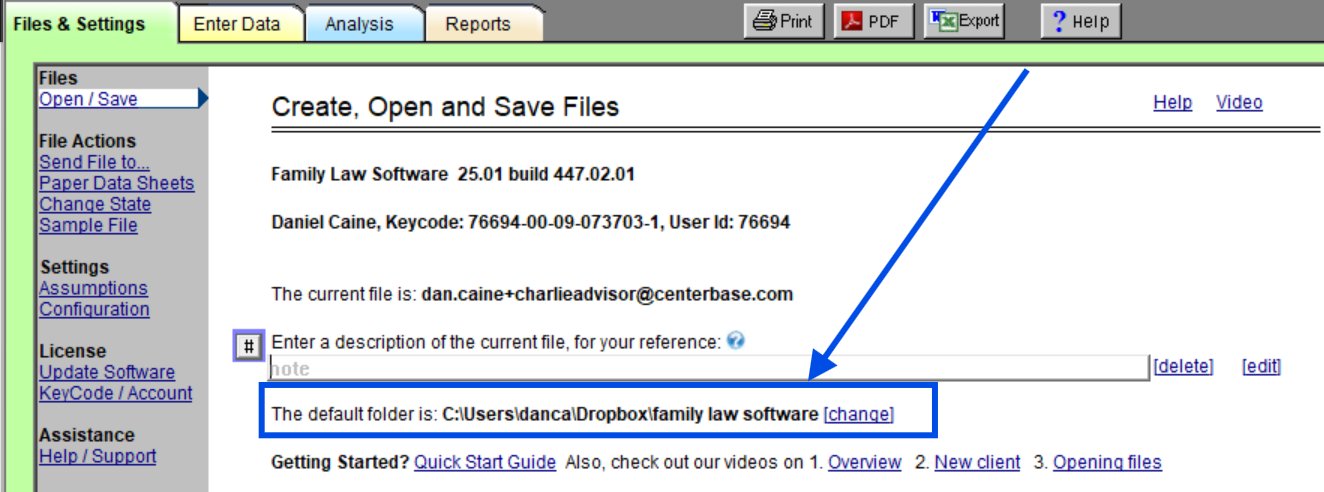

If the files are on your local hard drive only, find the folder where they are stored. To do this, look at the Files & Settings tab. You will see the location near the top of the screen, as shown below:

In the image above, the current folder is “Family Law Software” within a Dropbox folder.

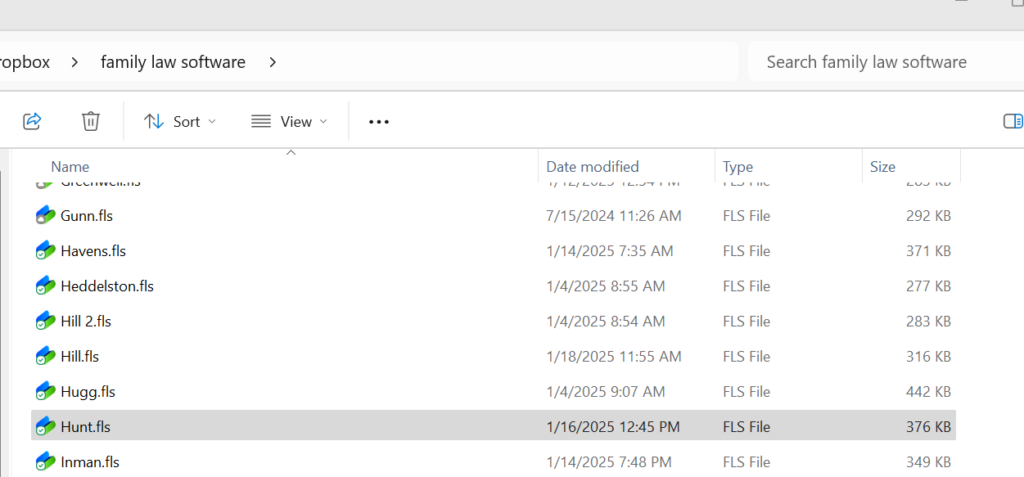

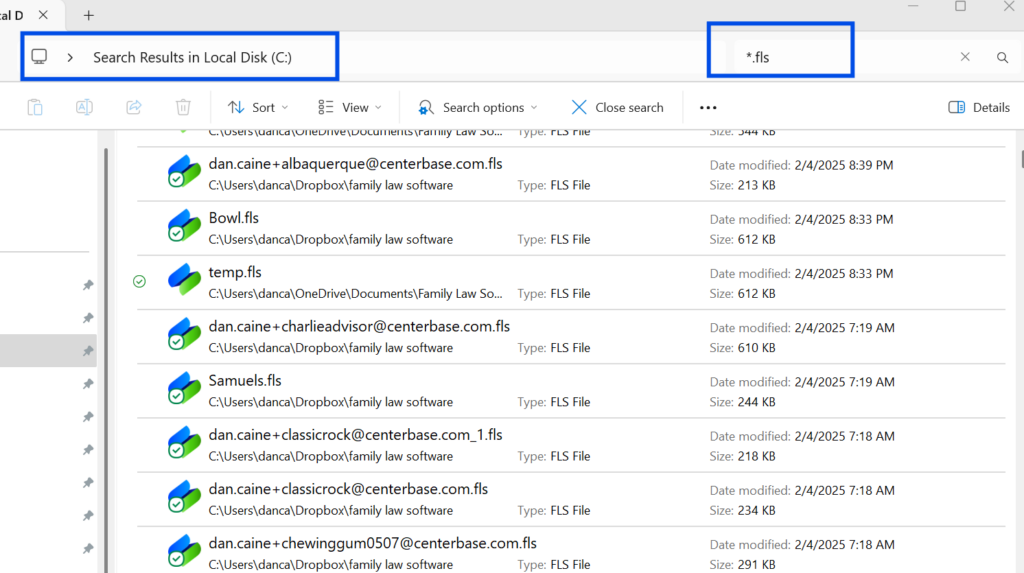

Close Family Law Software, and use Windows Explorer to navigate to the folder that was shown. All of the Family Law Software data files have the extension “.fls,” as shown below. (Your display may look different, depending on the display options in Windows Explorer.)

Copy those files to a place you will be able to access from your new computer. (If you have questions how to do that, search in your browser for “how to move files from one computer to another.”)

If the files are already external to your computer — such as on a Dropbox, Google Drive, OneDrive, or network drive — you can skip this step.

2. Additional Instructions for Macintosh.

If you can find your files using Finder, then follow the steps above.

If you can not find your files using Finder…

Click here for an FAQ on creating a folder you can locate using Finder

Once you create that folder, it may be necessary to open the existing files one at a time and then save them into that folder using “Files tab > Save As…”

You can click Files & Settings tab > Restore, and restore the most recent version of each file. They will go into your new default folder. You can change the name on each one to delete “_Restored” before they are saved.

Once all the files are all in a place you an access using Finder, close Family Law Software, and use Finder to drag the files to a place you will be able to access from your new computer.

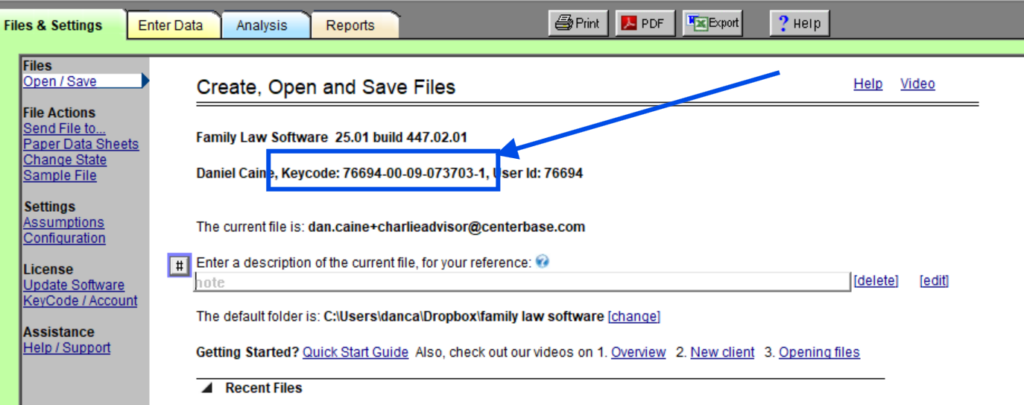

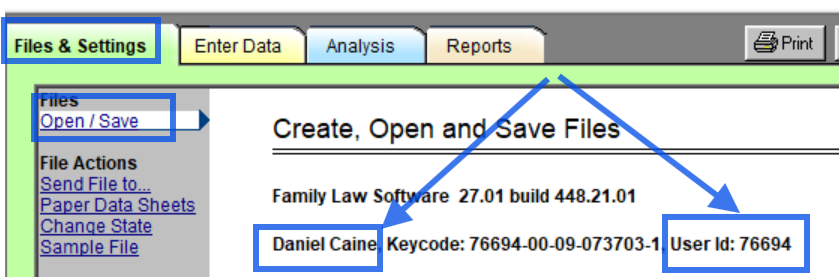

3. Write Down Your KeyCode.

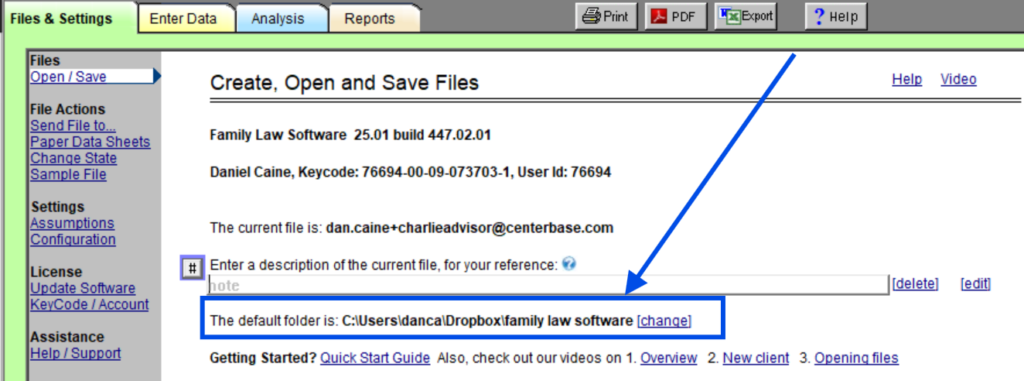

You can find your key code on the old computer on Files & Settings > Open/Save, as shown below.

Write it down. (If you can not do this, it is OK. Keep going.)

3. Install the software on the new computer.

To install the software on the new hard drive, click here:

Click here to download the latest version

After you download the software, run the downloaded file (click on it) to complete the installation.

4. On your new computer, start Family Law Software and set the default folder.

Double-click the Family Law Software icon on your desktop (illustrated below).

When Family Law Software starts for the first time, you will be asked for the default folder.

If you are using the software on a network, specify the default folder to be the folder on the network you are currently using.

If you are using Dropbox, Google Drive, OneDrive or a similar cloud-based folder, specify that.

If you are not using a network folder, perhaps you would want to take this opportunity to do that.

If you are running the software on Macintosh, we recommend that you set a folder you can find in Finder, Dropbox, Google Drive or similar cloud-based folder.

Click here for an FAQ on creating a folder you can locate using Finder

Or, accept the default option, which is the Documents > Family Law Software folder on the local hard drive.

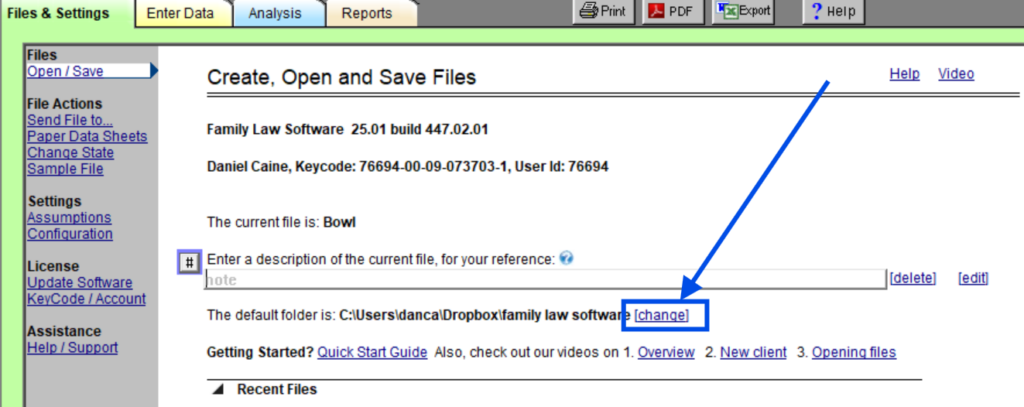

(You may change the default folder at any time, by clicking “Change” where the folder is shown on the Files & Settings screen, as shown below:

The first time you start Family Law Software, you will be asked for your email address.

You may also be asked to set an online password, which is used for client data entry, sending files to tech support, and other online-integrated features.

The software will attempt to download your KeyCode.

If that does not work, please search your email from Family Law Software for the word “KeyCode.”

If that does not work, you may e-mail us at support@familylawsoftware.com to request your KeyCode.

5. Move your existing files over.

If you have a network, or you are using Dropbox, Google Drive, OneDrive or a similar cloud-based folder, and the files are still there, there is nothing to do in this step.

Otherwise, if you backed up the files, drag them into your new folder on your new computer, using Windows “My Computer” for Windows or Finder for Macintosh. The files you want are those that end with “.fls”.

If you are storing client files in client folders, drag the client folders over to your new default folder.

6. That’s it.

You should be all set on your new computer.

If you have any questions, please do not hesitate to contact us.

.

If you are a lapsed subscriber, an inactive subscriber, or a subscriber who canceled, and you wish to resume your subscription or restart your subscription, welcome back!

Here is how to resume your subscription with the same account (so you can see your case files):

If you are using Cloud software (most subscribers):

- Log in at pro.flsgo.com. If you do not remember your password, click Forgot Password.

- You will be taken to the Account Manager.

- Click the tile to Restore Account.

If that does not work for you, or if you are using the desktop software:

- Search your email for an email labeled “Receipt for Family Law Software.”

- Open the invoice in the email and on one of the lines, you will see your User Id.

- Go to our Account page, and click the button for either Annual or Monthly subscribers.

Follow these steps:

1. Make sure your KeyCode file is named keycode.lst

2. Create a folder on the server for the file to reside in. You can create the folder in the same directory that the program installed in, or another folder as long as it is accessible to be read by Family Law Software when it starts up. Give the folder any name you like. “FLS Admin,” for example, is fine.

3. Place the keycode.lst file into the folder you created in step 2 above.

4. Create a plain text file (e.g., using Windows Notepad) called flsadmin.ini, with the following content (assuming you placed the keycode.lst file into the folder c:\temp):

[ADMIN]

AdminKeycodeFolder=c:\temp\

5. Copy this file to c:\program files (x86)\Flsplan\

6. Install the Family Law Software program to the server (unless you previously installed it).

7. Start Family Law Software and click Home tab > System Info > Click here to set System Administrator Options.

8. A dialog will open. Find the option for “Master KeyCode List.” Click “Browse,” and Navigate to the folder you just created. Click OK.

9. On your server, create a folder client files. This folder should be accessible to all users with full read/write permissions for all users. Name the folder anything you like. “Family Law Software Files,” for example, is fine.

10. Return to Family Law Software. On the Home tab > Sytem Info screen, click “Click here to specify Default Folder.” Navigate to, and select, the folder you just created.

11. To test: Click Files tab > New. Create a file and enter some data. Exit Family Law Software. Start Family Law Software agan, and click Files tab > Open. You should see the file. Open it. If your data is there, you are all set.

You, or your paralegal or assistant, may download the desktop software here:

Click here to download Family Law Software

When the software first starts, it will ask for a name and email address.

Enter the name and email of the licensed professional — not that of the paralegal or assistant.

If you need a KeyCode, search the professional’s email for “Family Law Software KeyCode.” If you can not find it, you can email us at support@familylawsoftware.com to ask.

Use the same password to log in on both computers.

You should also make sure that every computer’s Family Law Software folder for storing client files is the same.

That way, you will be able to work on the same files.

For more information on storing files, click the links shown below:

Where can I store client files?

How can I access files from anywhere (the Cloud)?

To configure Family Law Software to work in the Citrix environment, you will want to adjust the software’s Administrative Settings:

There are two folders to set up:

1. A “working folder” for information identifying the attorneys; and

2. A “default folder” for client data.

Attorneys need full read/write access to each folder. We discuss each folder below:

1. Networking folder.

a. Create a folder on the drive where that you wish to store the information that will identify the attorneys. In Family Law Software, we call that the “working folder.” You can name it, for example, “Family Law Software Working.”

b. Download and install Family Law Software.

Click here to go to the download screen.

c. Open the software and click Files & Settings > Configuration > System Administrator Options.

d. In the Administrator Settings dialog, enter the Working Folder in the section entitled “Central Server Configuration.”

e. Click the OK Button

f. You will see a confirming dialog. Click “OK.”

g. Your Working Folder is now set up.

2. Default Folder.

Create a folder on the server for client data. You might call it “Family Law Software Client Files.” Be sure that users will have full read/write access to the folder.

Start Family Law Software, and click Files & Settings, and change the default folder, as shown below.

Navigate to the folder you created above.

3. KeyCode File

Next, you will need a file called “Keycode.lst.”

Get this file from Family Law Software. Request it from tech support (support@FamilyLawSoftware.com).

The KeyCode.lst file will identify each licensed user.

When you get this file, return to the Administrator Settings dialog (illustrated above). Enter a path for the KeyCode file under the heading “Master KeyCode List.” Typically, this path will be the the folder where the program is installed.

Then place the file in that folder.

At this point, you should be all set up.

Most likely, the program is currently running, or it is still in memory from an earlier time running or from an earlier attempt to install.

If the program is currently running, simply exit the program and then click “Retry” on the installation dialog. If you have already clicked “Abort” on the installation dialog, just try installing again at this point.

If that does not work, you can start Windows Task Manager, by right clicking in the Task Bar, and selecting Task Manager. Then find any or all of the Family Law Software, FLSPlan and FLSPro processes, and remove them from memory. Then go back and click “Retry” on the installation dialog. If you have already clicked “Abort” on the installation dialog, just try installing again at this point.

If that does not work, or you could not figure out Task Manager, the next thing to try is click “Abort” on the installation dialog, restart your computer, and download and install Family Law Software again.

If that does not work, it may be that you do not have the administrative permission to save information (“write”) on the hard drive. In that case, speak with the office administrator about what to do next. For example, you may be able to log in to the computer as an “Administrator,” which would allow you to install the software.

Most likely, this message is generated by your anti-virus software. We have seen this especially with the free programs.

Just temporarily turn off the anti-virus software and start the program normally.

If you do not know how to turn off the anti-virus program, ask your IT person, check the anti-virus company’s web site, or call the anti-virus company’s tech support.

Typically, you are having this problem because of a corporate firewall.

Unfortuantely, if your corporation’s firewall is blocking e-mail from going out from Family Law Software, there is nothing we can do to get the e-mail to go out.

However, you do have an alternative.

Anything that we send from within the program, you can send as an attachment.

1. Documents.

First, print the document to a PDF, by clicking the PDF button at the top of the screen.

To send a PDF to a client or to another professional, go to your regular e-mail program, address an e-mail to the recipient, and simply attach the PDF.

Look for the PDF in your Family Law Software current folder.

The PDF may be in a folder with the client’s name within the current folder.

2. Client data file.

Similar to PDF, you can attach the client data file to an e-mail.

The client data file will also probably be in your current folder, or in a folder with the client’s name within the current folder.

It has the exetnsion “.fls” at the end of the file name.

The recipient will only be able to open the Client Data file if he or she has Family Law Software (including a trial edition).

Search your email for “Family Law Software KeyCode.”

If you do not find it, we can look try to look up your KeyCode for you. Do the following:

1. Start Family Law Software.

2. Click Files & Settings > KeyCode/Account > New KeyCode > Get Keycode.

If that does not work, contact us to ask.

This may be a permissions/security problem.

You may be able to fix it with the following steps:

1. Open Windows Explorer. You can do this by holding down the Windows key and pressing the letter “E.”

2. Navigate to c:\Program Files (x86)\FLSPlan. Do this by finding the folder icon labeled “Hard Drive C:” (or similar language) and double-clicking it. Then find the folder icon labeled “Program Files (x86)” and double-clicking that. Finally, find the folder icon labeld FLSPlan, and double-click that.

3. Find the file named FLSPlan.exe.

4. With your mouse, right-click that file.

5. A menu will pop up. Select “Run as Administrator.”

That may fix the problem.

If not, please contact technical support.

Click here to e-mail technical support

If you are using the desktop software and would like to upgrade to a Cloud edition, please do the following:

- Search your email for “Receipt for Family Law Software.”

- In that email you will find your User ID.

- Click here and click the button to Upgrade. (You will need your User Id.)

If you are using the Cloud Edition and would like to upgrade to the Firm Edition, please do the following:

- Log in at pro.flsgo.com.

- In the top right hand corner of the screen click the Account button. This will open the Account Manager.

- Click the tile to upgrade.

If you have the Basic Edition (which is both desktop and Cloud), and you would like to upgrade to get the full-featured software (including Analysis and Reports), please do the following:

- If you are using the Basic Edition on the desktop, follow the instructions above for using desktop software.

- If you are using the Basic Edition on the cloud, follow the instructions above for using the Cloud software.

Apple has announced that it is considering stopping support for Intel processors on Apple PCs.

Apple has been including its own Apple silicon processor in its computers starting in 2020 through 2023 (depending on model).

Family Law Software is running fine on those computers and it will continue to do so.

And even if you do have a computer that uses Intel processors, as long as the computer is running, Family Law Software will run on it.

You may not be able to get the latest operating system upgrades, but otherwise you will be fine.

This is NOT a trojan. The identification by Malwarebytes is a “false positive.” Here are the steps to follow to let Malewarebytes know this::

1. Start Malwarebytes. Right-click the icon, and select Open Malwarebytes Anti-Malware.

2. Clear all checkboxes next to Debenu items.

3. Click “Next”

4. Select “Ignore Always.”

Follow the steps below, and we will restore as much as possible.

1. Reinstall the Software.

Getting the software re-installed is the easy part. You can click here and download it:

Download latest version of Family Law Software

2. Enter your email and password.

3. Restore your files.

This part is a bit more involved, and it may not work.

The software and client files are stored on a network in your office, in the cloud, or on your computer.

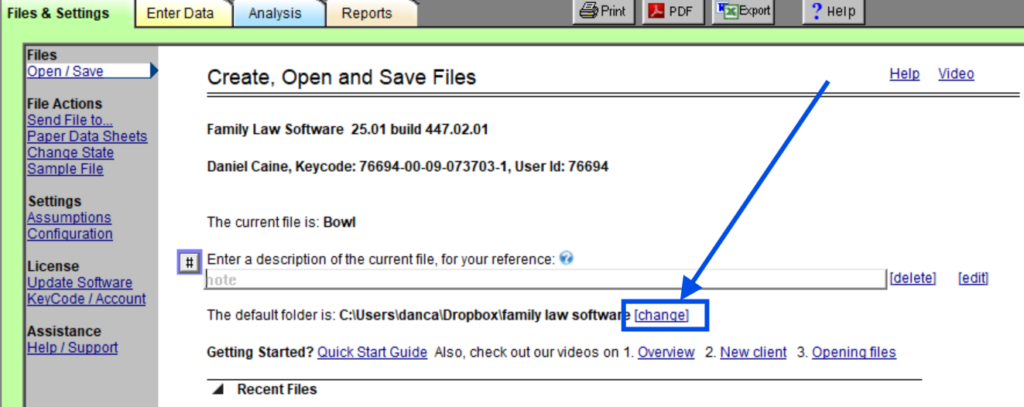

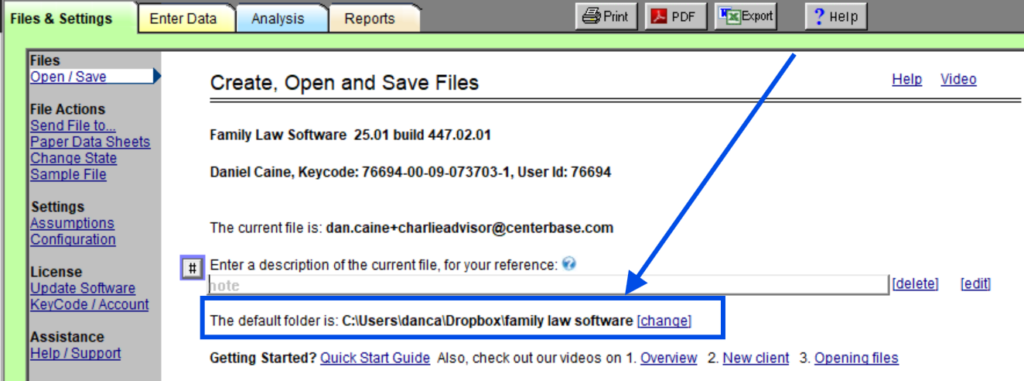

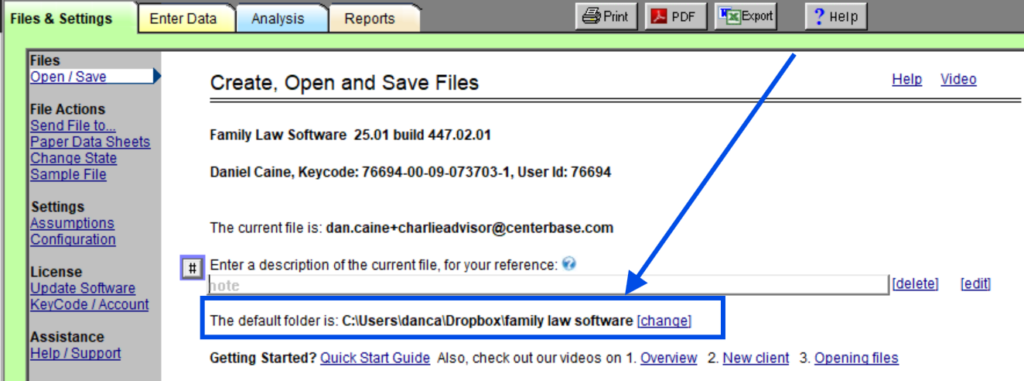

If you have an office network, they were probably stored in a folder on your office network. In that case, the files are probably all still there. All you have to do to point the program to that folder. To do that, click Files & Settings > [change], as shown below.

Similarly, if the files were in the cloud, with DropBox, OneDrive, or Google Drive, for example, do the same thing and navigate to the drive in the cloud.

If you do not have a network, the files were probably saved on your hard drive in the folder My Documents > Family Law Software.

You should retrieve them from that folder in your office back-ups.

The files have the name you gave them, and then “.fls.”

You can use Windows Explorer (Windows key + E) or Macintosh Finder to drag the folders into the folder where you want them now.

If you saved the files only on the computer that crashed, and you have no back-ups, we are sorry to tell you that there is no way to recover them.

For the future, be sure you have backups!

If you were sent a link to register your software, create an account, and set your password, and that link has expired, do the following:

If you are a professional (Attorney or Financial Planner), go to pro.flsgo.com and click Forgot Password.

If you are a client, go to client.flsgo.com and click Forgot Password.

If you are an individual using the software for your own case, go to my.flsgo.com and click Forgot Password.

If the email address you enter is in our system, we will send another registration link to that email address.

If not, please contact us and let us know the name and email address you would like to register.

If you get this message and you are a licensed subscriber, here are the things to try:

1. Re-enter your KeyCode.

You should have received your KeyCode from us by e-mail.

If you know your KeyCode, do the following:

1. Start Family Law Software.

2. Click Files & Settings tab > KeyCodes / Account > New KeyCode.

3. Enter your name and KeyCode with the dashes.

2. Find your KeyCode.

If your subscription is still current, but you don’t have your KeyCode, do the following:

1. Start Family Law Software.

2. Click Files & Settings > KeyCode / Account > New KeyCode > Get KeyCode. We will try to put the KeyCode into your software for you.

3. If that does not work, contact us to request your KeyCode.

3. Renew your subscription.

If your subscription is not current, you may need to renew it.

Click here to renew your subscription.

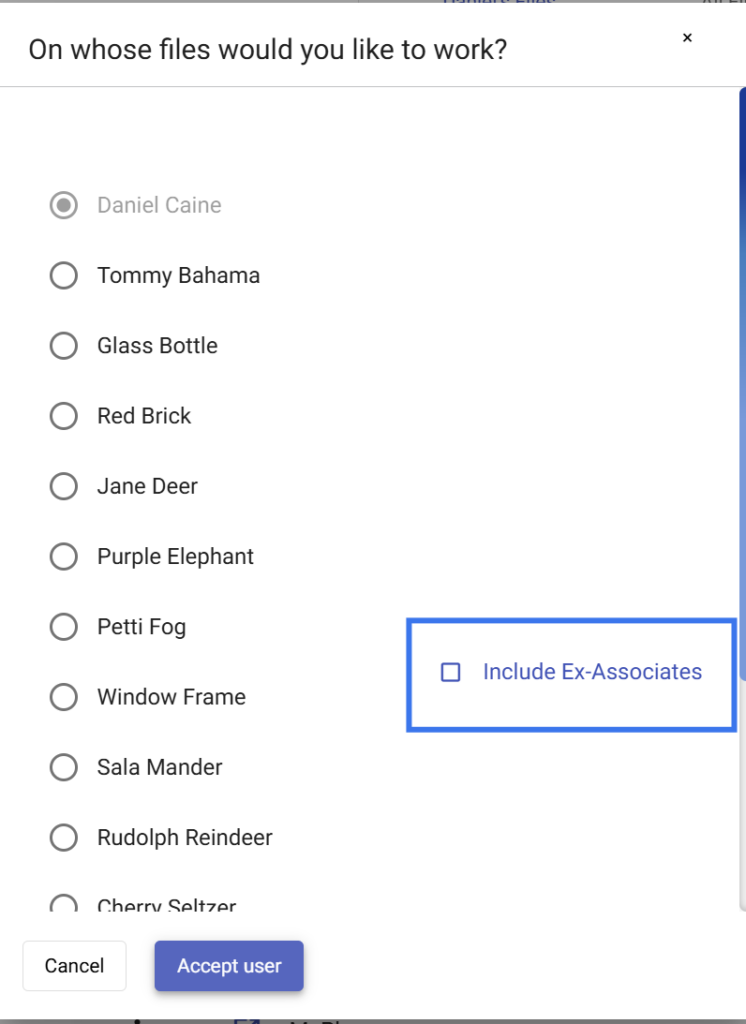

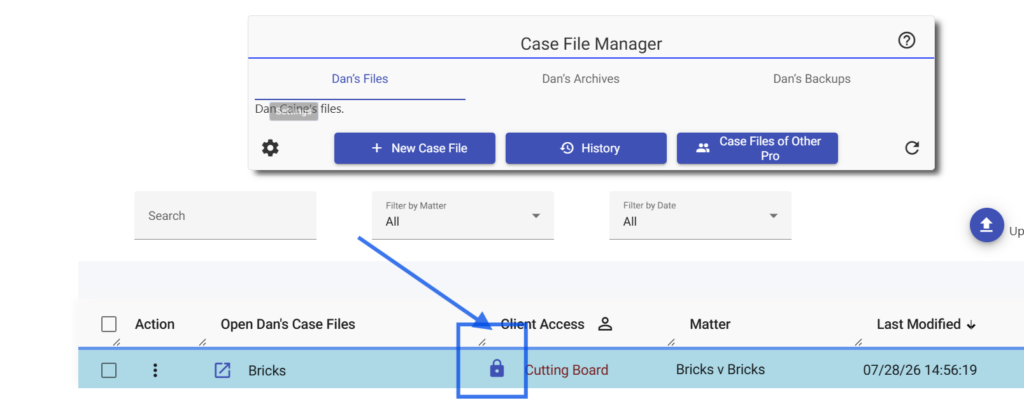

If you have the Firm edition of the software, members of the firm may open the files of former members.

This includes former associates, ex-associates, partners who have left the firm, etc.

Here’s how:

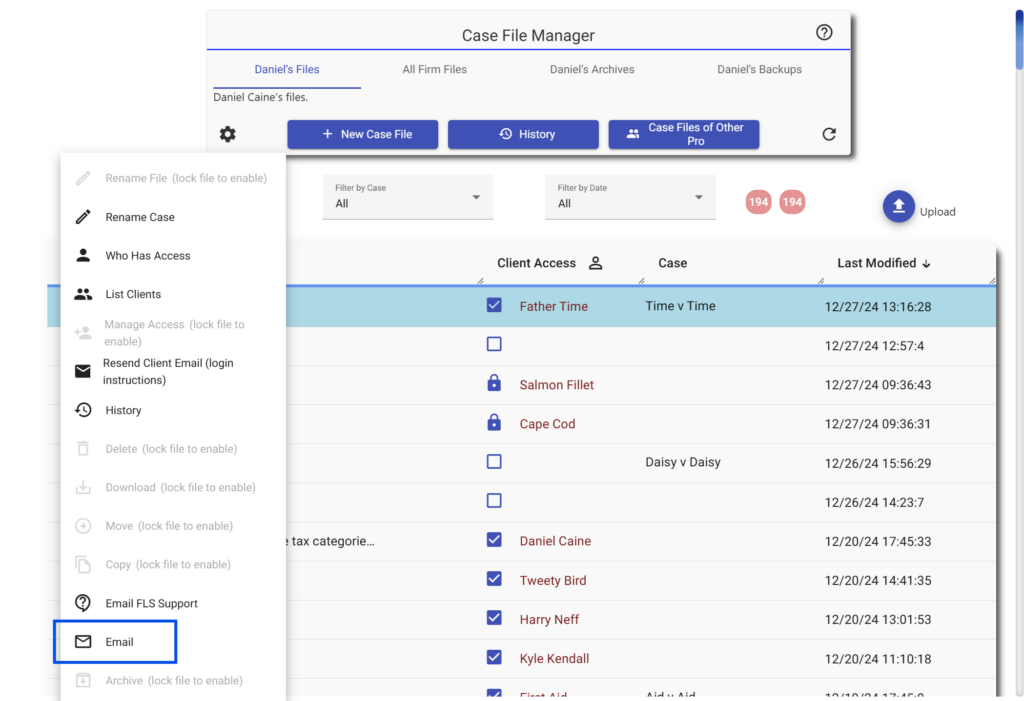

In the File Manager, the person who wants to open the file should click “Case Files of Other Pro” (top right) and then check the box to include ex-associates. (That term is used generically and includes partners.)

The image below will illustrate:

The list will then include former associates and you may open their files to view and edit.

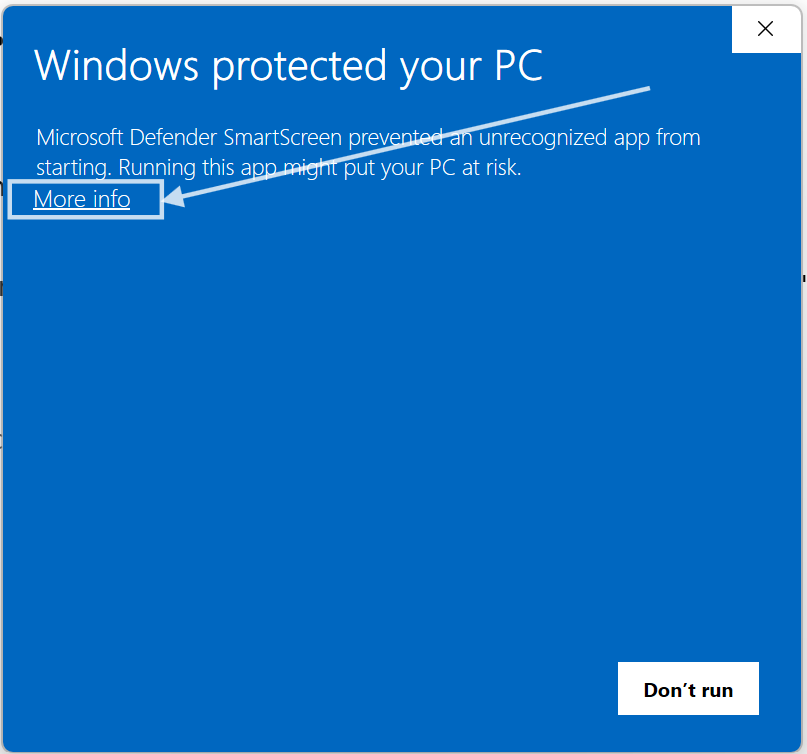

You may see the screen shown below when you install the Windows download.

There is no virus or malware in Family Law Software.

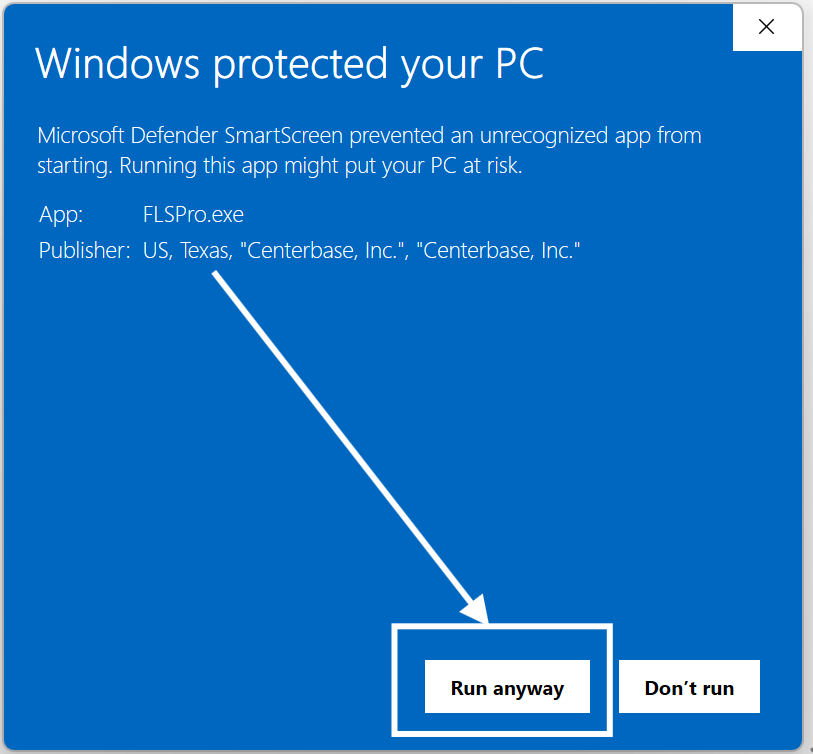

Here are the steps to safely install the app:

- Click the “More info” link, as shown above.

- Click the “Run anyway” button, as shown below.

- Continue with the installer as usual.

Again, this is perfectly safe.

The error is on Microsoft’s part, not recognizing the validation code that is correctly built into the installer.

The app itself is fine, and your PC will not be harmed.

If you would like to take steps so that you do not see this message again in the future, please do the following:

In your Taskbar, in the “Search” area, type “Command prompt.”

In the pop-up that appears, on the right, select “Run as administrator”

A box will appear that looks something like this:

Cut and paste each of the following lines into the box that appears (one at a time):

cd c:\Program Files\Windows Defender

MpCmdRun.exe -removedefinitions -dynamicsignatures

MpCmdRun.exe -SignatureUpdate

Don’t worry if you see an error message.

You should be all set and should not see the Windows Defender message again.

Macintosh-Specific questions

Here are the steps to remove Family Law Software from your Mac computer.

To remove the program but NOT the data, skip the last step.

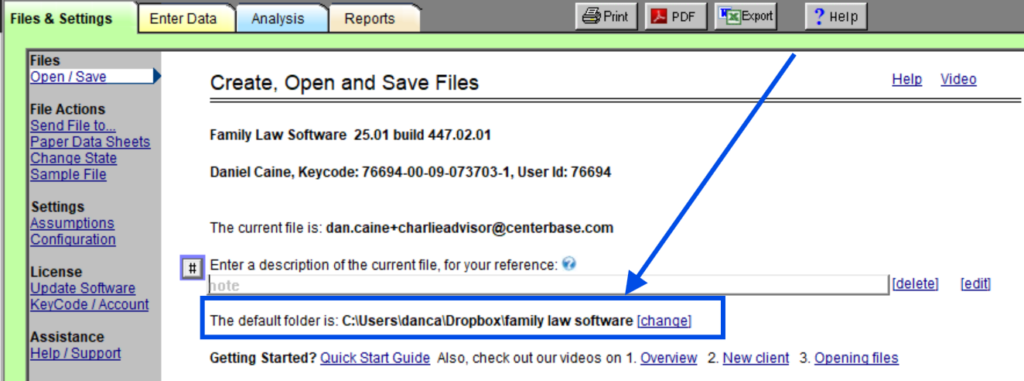

1. If you are going to delete the data at the end, determine where your files are stored. You will see the location if you start Family Law Software, click Files & Settings, near the top, after the words, “The default folder is:….”

2. Close Family Law Software, if it is open.

3. Start Finder.

4. Click on Applications.

5. Drag the Family Law Software icon from your Applications folder to the Trash. The Trash should change its appearance and make a crunching noise.

6. Verify that the icon is no longer in the list in the Applications folder. If it is still there, drag it to the Trash again.

7. In Finder, slect the Go menu at the top of the screen. Hold down the option key on your keyboard, and you will see an option called Library.

8. Select that option. Then, under Application Support, drag Family Law Software into the Trash.

9. This will delete the program, but NOT the data. If you do want to delete the data, drag your data folder into the Trash. Typically, this will be the “Family Law Software” folder from the Documents folder. Before you do this, please back the files up somewhere, so you can access them later. We do NOT have access to files located on your Mac computer, so we will not be able to restore them for you.

Please follow these steps, which we have found sometimes to be necessary, because the Macintosh’s download system does not always seem to be working correctly:

1. Delete Family Law Software. Drag the Family Law Software icon from your applications folder into the trash. If Family Law Software is in your dock at the bottom of the screen, also drag the icon from there into the trash. This will NOT affect your client files. Your client files will be untouched by this action.

2. Additional steps. Follow these additional steps to completely remove Family Law Software program (but not data files).

3. Restart your computer. Restart your computer. This resets the Macintosh’s download system, so the new file will replace the old one.

4. Download the latest Family Law Software. Download from our website, here:

Click here to go to the Download page

5. Minimize browser and drag icon. After the download completes, you need to minimize your browser (Safari, Chrome, Firefox, etc.), and drag the newly downloaded icon into the Applications folder.

6. Try a different browser. If it still is not working, try a different browser (Firefox, Safari, Chrome, etc.).

After the software is installed, you may drag the icon from the Applications folder to the Dock at the bottom of the screen.

Cloud Edition questions

If you are having trouble logging in, please try the following:

- If you are an attorney or financial professional, and you do not know your password, go to the login screen at pro.flsgo.com and click Forgot Password.

- If you are a client, go to client.flsgo.com and click Forgot Password.

- If that is not the issue, then, at the login screen, try entering your email address in all lower-case letters.

- If that does not work, please Contact Us. Let us know your email address and whether you are a professional, client, or individual.

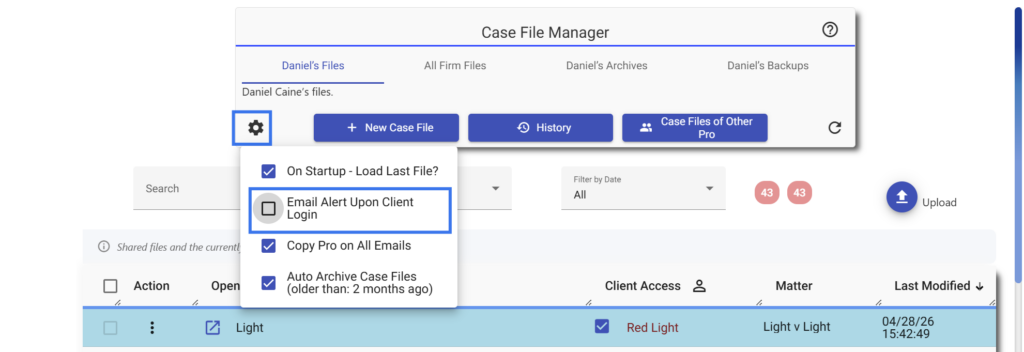

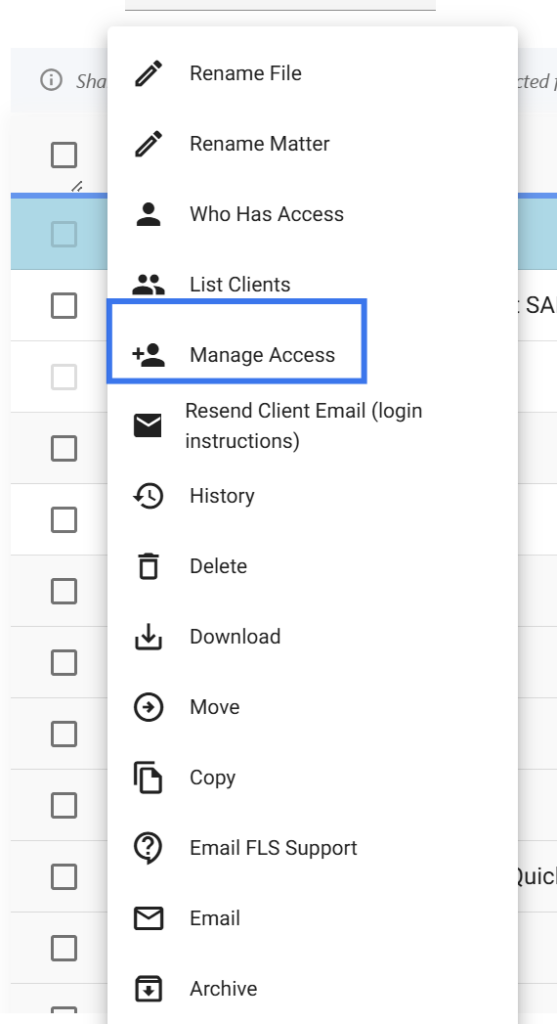

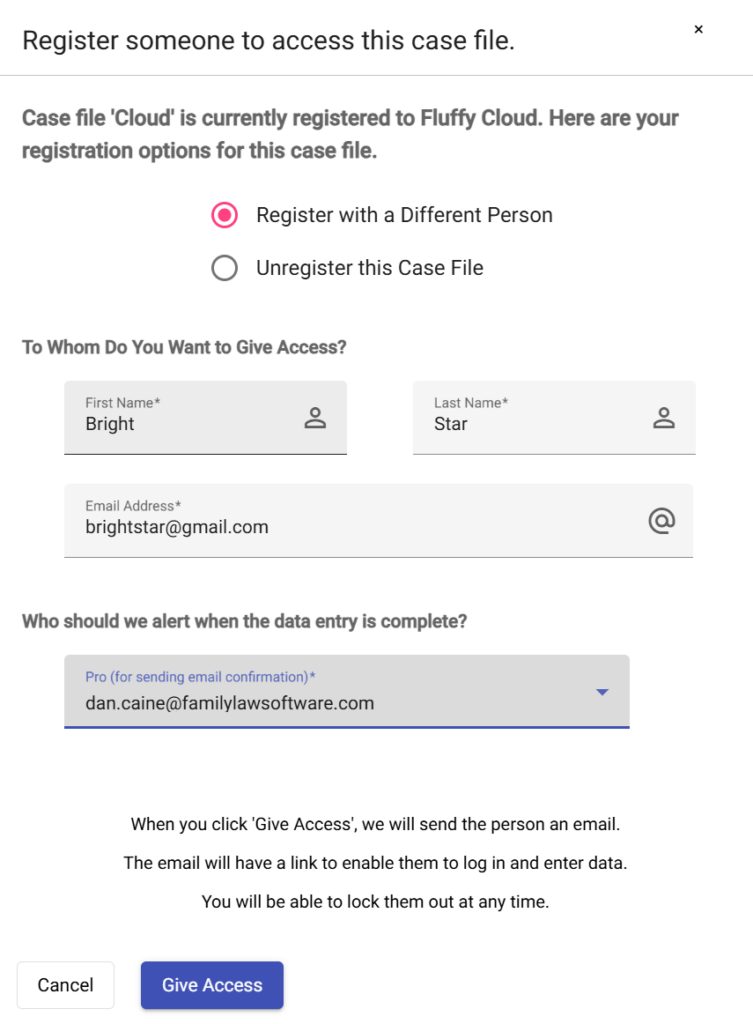

In order to keep you informed, Family Law Software automatically generates a number of emails regarding client activity.

Here’s how you can control who receives emails and which emails are sent.

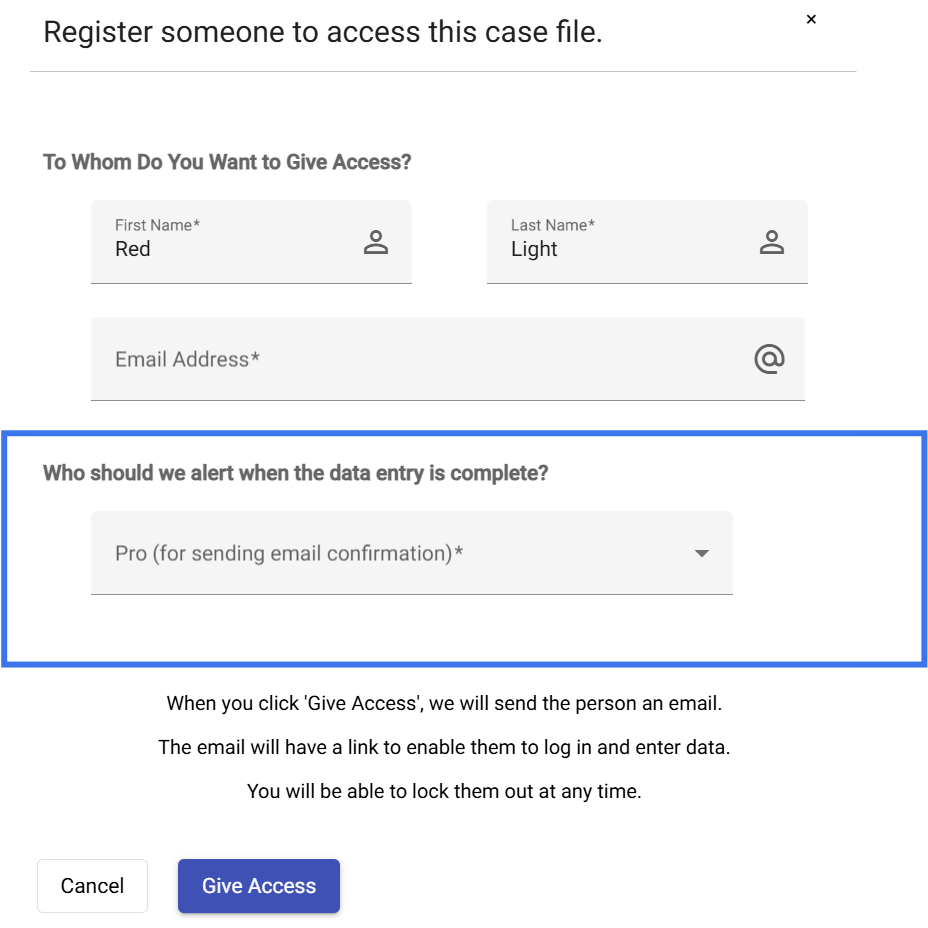

Who receives emails

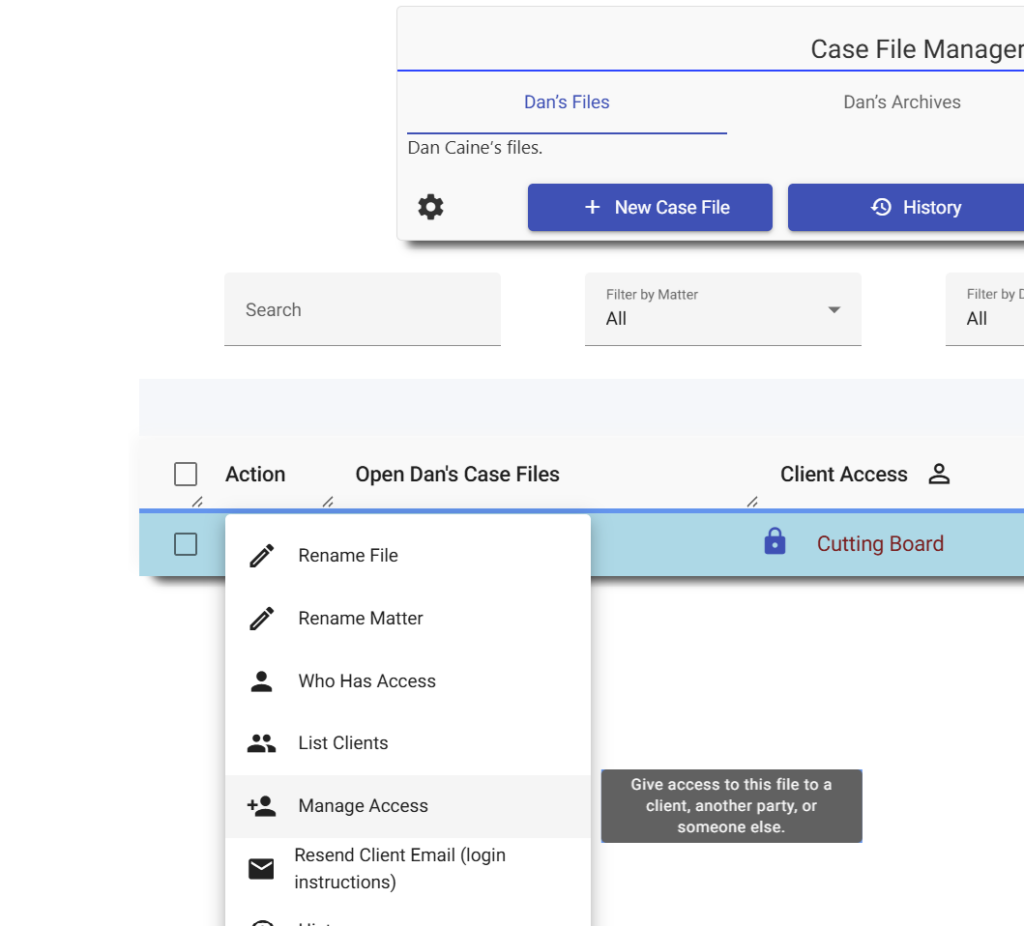

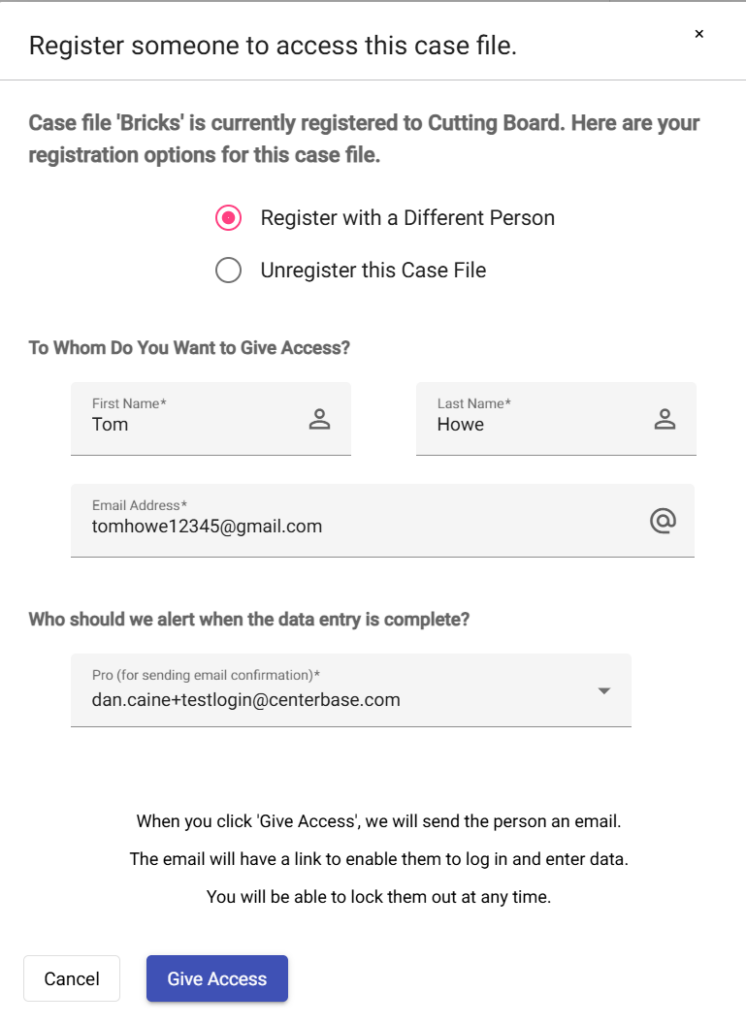

When you first grant access to a file to the client, you specify at that time which individual or staff member should receive emails regarding client activity, as shown below.

The person will receive all client related emails until you change that designation.

This FAQ explains how to change that designation.

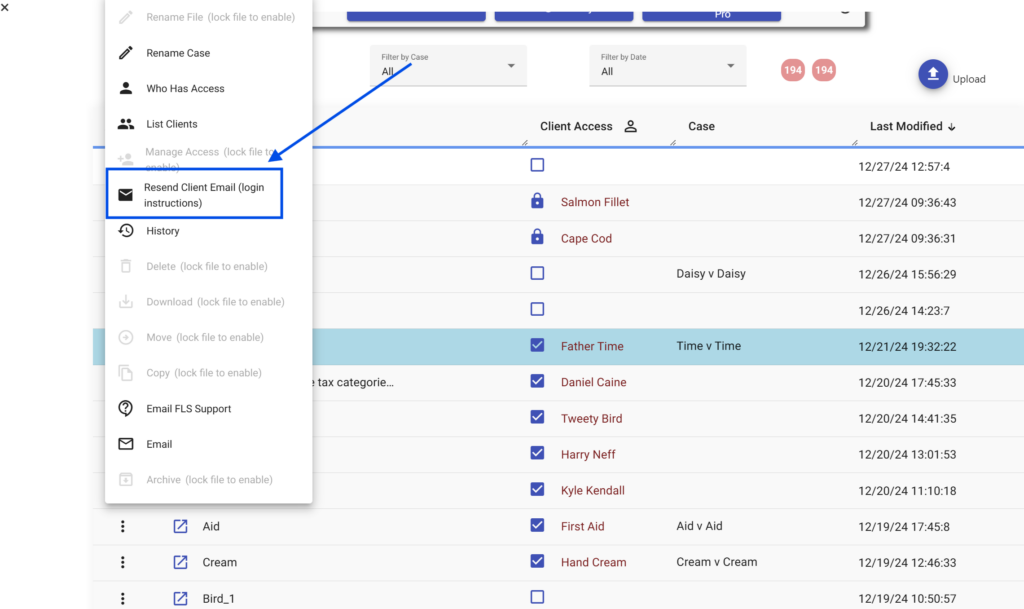

Email when client logs in

The software automatically generates an email when the client first logs in.

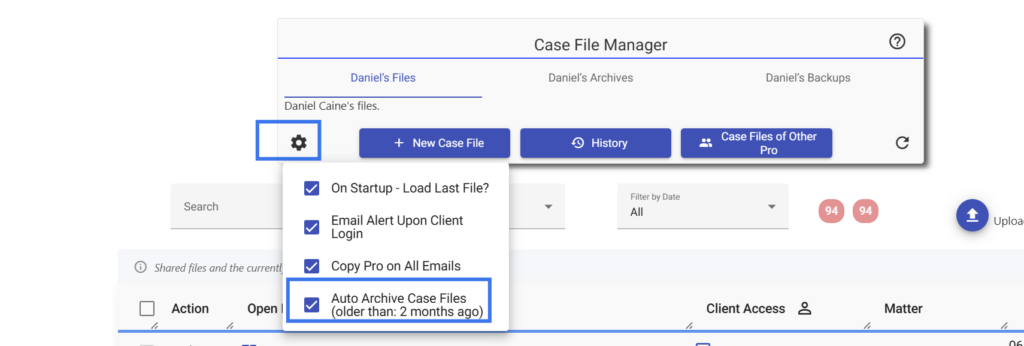

If you would like to not receive further emails, you can do that by specifying the settings shown below on the settings gear in the File Manager.

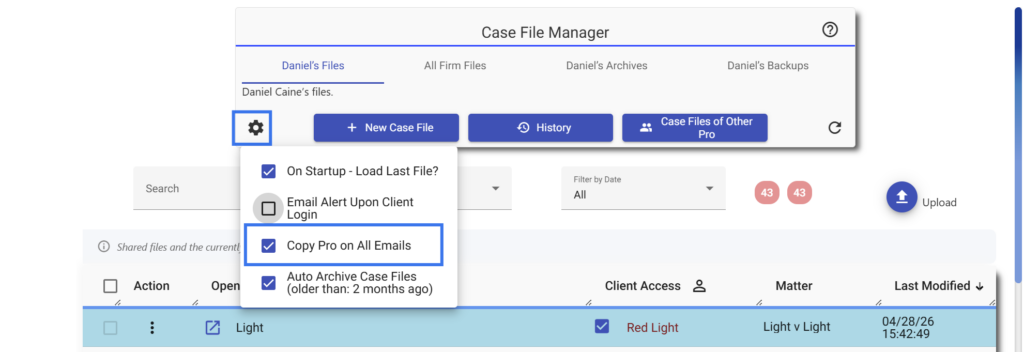

Email to professional

If you have the firm edition of the software, it is possible to specify that a staff member will receive the emails.

If you would like, you can also specify that the attorney or financial professional who is in charge of the case will receive the emails as well.

On the settings gear in File Manager, select the option to Copy Pro on All Emails, as shown below.

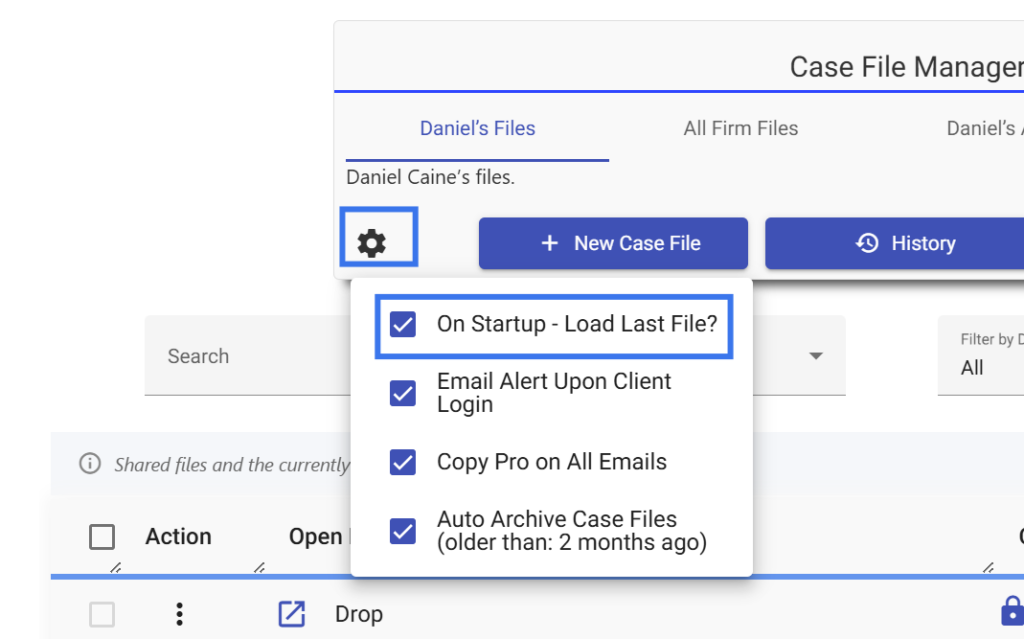

When the software starts, you have the option to either have the last file load automatically or to open to the File Manager.

You specify this option in the File Manager on the Settings gear as shown below.

If this option is checked, then, when you open the program, the last file you were working on will open up.

If this option is cleared, then, when you open the program, you will open directly into the File Manager and be able to select the file you want.

You may upload files from the Windows and Mac editions to the Cloud Edition and download files from the Cloud Edition to the Windows and Mac editions.

The easiest way to do that is from within the Cloud Edition.

To upload files from the desktop to the Cloud, you may do the following:

- Log in to the Cloud and click File Manager (top left).

- Click “Upload” (on the right).

- Navigate to the file on the desktop and click “OK.”

To download files from Cloud to desktop:

- Click File Manager (top left)

- On the line where the file is listed, click the three dots menu.

- Click Download.

You can also upload and download from within the desktop editions.

- Click Files & Settings > Open/Save.

- You will see buttons labeled Download, Upload, and sometimes Send Back.

- Read the help for each of those buttons for the appropriate action.

If you have many files, you must open them one at a time on your Windows or Mac desktop, and upload each in turn to the Cloud.

If you have uploaded a file to the Cloud or downloaded a file from the Cloud, you will end up with multiple versions of the file, one on the Windows or Mac desktop edition and one in the Cloud. Please be careful that you are always working in the latest version.

If you wish, you may delete the file from the Windows or Mac computer after you upload it to the Cloud (Files & Settings > Open/Save > Delete). This practice will assure that you have only one current version, and it will prevent you from entering some data in one file and other data in another file.

This FAQ will guide you in your transition from using the desktop software to using the Cloud software.

Differences in look and feel.

The main difference in look and feel is that the cloud software has all the tabs along the side, as shown below.

Also, the color scheme is slightly different, as you can see.

The fields on the screens and calculations are exactly identical between the two versions, however.

Logging In

For the cloud version, you’ll log in at pro.flsgo.com using your email address and a password.

You may change the password by clicking “Forgot your password?” on the login screen.

Enter you email address in all lower-case.

Similarly, if you have never logged in or do not know your password, just go to pro.flsgo.com and click “Forgot your password?” And, again, enter you email address in all lower-case.

Creating files

For all file-related activity, click the File Manager button in the upper left hand corner.

Clicking that button opens the File Manager as shown below.

When you first log in, the software will take you directly to the File Manager.

With the Firm Edition, if you are a paralegal or other staff member, you must click the button labeled “Case Files of Other Pro” in order to open a file.

Paralegals can create new files, but only after they have identified which professional they are working for by clicking “Case Files of Other Pro.”

Anyone with the Firm Edition can open the files of another member of the firm by clicking the button labeled “Case Files of Other Pro.”

Folders

There are no folders in the Cloud edition. However, you can quickly find the file you are looking for by clicking in the search box at the top and entering the file name.

If you give the case a name when you start the file, then you can enter the case name in the box labeled Search Filter by Matter.

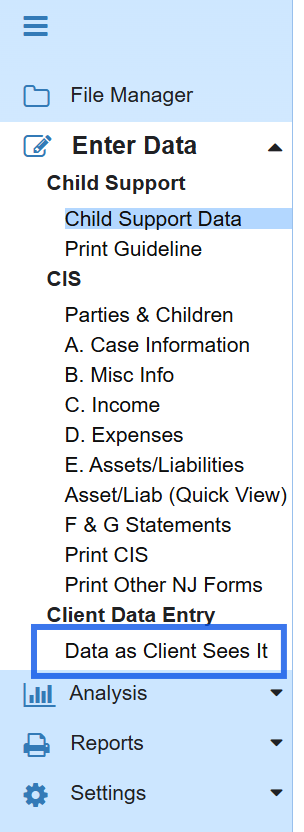

Client Data Entry

Client Data Entry is smoother with the Cloud Edition than with the Desktop.

To make the client data entry accessible to the client, just click the checkbox under the Client Access column.

To see what the client sees, open the file and along the left, click the link labeled “Data as Client Sees it,” as shown below.

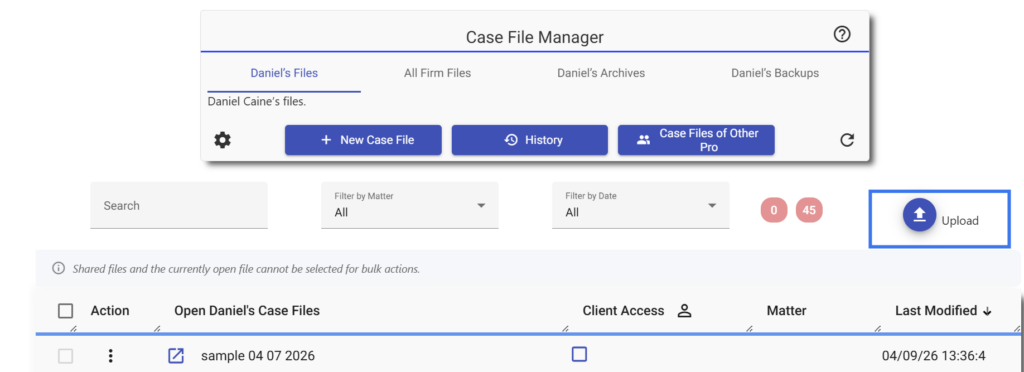

Uploading Files from the Desktop

You can upload files from the desktop by clicking the upload button near the top on the right.

For more information about the File Manager, please see the blog post that we wrote when we released it.

If you have multiple files in a single folder on the desktop, you will be able to upload them all at once.

If your files are all in different folders, you will have to navigate to each one and upload it.

In that case, you may wish to upload files only as you need them.

Emailing files to other Professionals

You can email a file to another professional. Here’s how:

- Open File Manager.

- On the line where the file is located, click the 3-dots button (in the Action column on the left).

- Select Email.

Printing

All printing in the Cloud Edition is done via PDF.

Open the page you want to print and click the PDF icon in the top right corner.

If you would like to edit the printed document, start Microsoft Word and open the PDF file from within Microsoft Word. Word will convert it to a Word document and you can edit it.

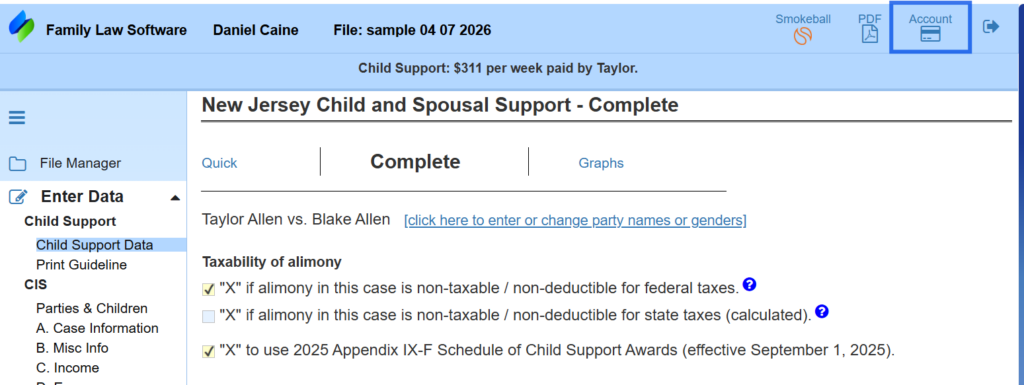

Managing Your Account

From within the Cloud Edition, you can make account changes by clicking the Account button in the upper right hand corner.

This will take you to our Account Manager, where you can do the following:

- Add or remove users to your account.

- Change credit card information.

- Change contact information.

- Set up 2-factor authentication (2FA).

- View your payments.

- Specify which employees may use the Account Manager.

- Upgrade your edition.

If you need to change your email address, please contact us.

Choosing Between Cloud and Firm Editions

The Cloud Edition is designed for individual practitioners. An attorney or financial planner may share the login with a paralegal or other staff, but with the Cloud Edition, only one person may be logged in at a time.

With the Firm Edition, each individual gets their own login, so all attorneys and all paralegals may be logged in at the same time.

The Firm Edition is designed for firms of two or more attorneys and situations where an individual attorney is working with two or more paralegals.

One big advantage of the Firm Edition is that all of the paralegals and staff get licenses to log in at no additional charge.

As indicated above, the Firm Edition also allows an attorney in the firm to open the files of any other attorney.

More Questions

Click here for answers to questions relating to our phasing out of the desktop software, the transition for Smokeball users, and more.

If you can’t open a file, please try the following:

- Confirm that you are using a supported browser – Firefox or Google Chrome. If not, please try one of those browsers.

- If you are using Chrome or Firefox, and you are still having an issue, please try opening a browser tab in Incognito mode and trying again.

- If you are using a VPN (virtual private network), you may also want to test outside of the VPN. Test on your phone, or try turning the VPN off temporarily.

- If none of the above solves the issue, please send a screenshot of what you are seeing and let us know which browser you are using. Use our Contact Us page.

As you may know, Family Law Software is phasing out the desktop software on September 30, 2026.

This FAQ will answer questions that Basic Edition users may have about their next steps.

Confirming Your Edition

If you are not sure what edition you have, you can find out by clicking here, filling in the account information, and clicking Submit Request. (No charge at that moment.)

You can find the person whose name is on the account, and their User Id, either of the following ways:

1. In the Desktop software, look at the top of the Open / Save screen, as shown below; or

2. In the Cloud software, look at the very bottom of the screen, as shown below:

Confirming the Edition You are Using

Basic Edition subscribers may use either Cloud or desktop, so you may not know which edition you are using. To determine which edition you are using, look at the screen images below.

This is the desktop:

This is the Cloud:

Looking at these images will tell you which you are using.

If you are using the desktop, you will need to transition to the Cloud.

If other people in your office are using the desktop, they will need to transition to the Cloud.

Logging In to Cloud

If you have the Basic Edition, the person whose name is on the account may already log in to the Cloud.

If the person whose name is on the account is not currently logging in to the Cloud, all they have to do is to go to pro.flsgo.com and click “Forgot your password?”

That will allow them to reset their password. Then they can go to pro.flsgo.com and log in any time.

Transitioning to Cloud

If you are currently using the desktop software, then you will want to transition to using the Cloud.

Click here for help transitioning to using the Cloud.

Considering Firm Basic

Most of our Basic Edition firms have only one subscriber.

If there are more people in the firm who would like to access the software, you may wish to consider upgrading to the Firm Basic edition.

The firm basic edition gives the following benefits.

- Add all additional staff, each with their own logins, at no additional cost.

- Enable professionals and staff to view and edit each other’s files.

- Enable opening of files of professionals who have left the firm.

The Firm Basic edition costs $10 more per professional per month than the Basic Edition.

To upgrade to the Firm Basic Edition:

- Click here.

- Enter the name, state, and User Id as shown above.

- Click Submit Request.

- Select Firm Basic and continue.

As an alternative, you can have multiple Basic Edition subscribers on the same account, but they will not be able to see each of these files and you will not be able to add staff.

If there is only one person in the firm, then Basic Edition is the way to go. If more than one person wants to work in the software, however, then we really recommend Firm Basic.

Add Additional Members

If you upgrade to Firm Basic, you can add additional members through the Account Manager as follows:

- Log in to Family Law Software.

- In the upper right hand corner, click the Account button.

- Click the tile to Add/Remove Employees.

- Click the “+” button for each employee you wish to add.

Additional professionals will add $10 per month to your charge. Additional non-professional staff, such as paralegals, are free.

Add a System Administrator

When you add an employee, specify that they are a system administrator.

The person will then be able to log in themselves and add and remove employees.

If they do not get a registration email, they should do the following:

- Go to pro.flsgo.com.

- Click “Forgot your password?”

- Register.

- Go to pro.flsgo.com again.

They will be taken to the Account Manager.

Questions?

Click here for general questions about phasing out of the desktop software.

As you may know, Family Law Software is phasing out the desktop software on September 30, 2026.

This FAQ will answer questions that Cloud Firm Edition users may have about their next steps.

Confirming the Edition You are Signed Up For

If you are not sure what edition you have, you can find out by clicking here, filling in the account information, and clicking Submit Request. (No charge at that moment.)

You can find the person whose name is on the account, and their User Id, by logging in to the Cloud software and looking at the very bottom of the Cloud screen, as shown below…

… or starting the Desktop software and looking at the top of the Open / Save screen, as shown below.

Confirming the Edition You are Using

Cloud Edition subscribers may use either Cloud or desktop, so you may not know which edition you are using. To determine which edition you are using, look at the screen images below.

This is the desktop:

This is the Cloud:

Looking at these images will tell you which you are using.

If you are using the desktop, you will need to transition to the Cloud.

If other people in your office are using the desktop, they will need to transition to the Cloud.

Logging In to Cloud

If you have the Cloud Firm Edition, all the licensed professionals and staff may already log in to the Cloud.

If the person whose name is on the account is not currently logging in to the Cloud, all they have to do is to go to pro.flsgo.com and click “Forgot your password?”

That will allow them to reset their password. Then they can go to pro.flsgo.com and log in any time.

Who is Licensed?

To find out who is licensed, the person whose name is on the account (see above) can use the Account Manager.

To do that:

- The person whose name is on the account should log in.

- Click the Account button in the upper right hand corner.

- Click on the tile to add and remove employees.

- Click the “+” button to add each employee.

You will then see a list of all the people who are licensed.

At this point, you may add and remove professionals.

You can also add and remove staff such as paralegals, billing administrators, system administrators.

These staff members are free. You may add as many as you would like at no additional charge.

Add Additional Members

If you upgrade to Cloud Firm, you can add additional members through the Account Manager as follows:

- Log in to Family Law Software.

- In the upper right hand corner, click the Account button.

- Click the tile to Add/Remove Employees.

- Click the “+” at the top to add employees

Additional professionals will add $10 per month to your charge. Additional non-professional staff, such as paralegals, are free.

Add a System Administrator

When you add an employee, specify that they are a system administrator.

The person will then be able to log in themselves and add and remove employees.

If they do not get a registration email, they should do the following:

- Go to pro.flsgo.com.

- Click “Forgot your password?”

- Register.

- Go to pro.flsgo.com again.

They will be taken to the Account Manager.

Transitioning to Cloud

If you or members of your firm are currently using the desktop software, then you and they will want to transition to using the Cloud.

Click here for help transitioning to using the Cloud.

Questions?

Click here for general questions about phasing out of the desktop software.

As you may know, Family Law Software is phasing out the desktop software on September 30, 2026.

This FAQ will answer questions that Cloud Individual Edition users may have about their next steps.

Confirming Your Edition

If you are not sure what edition you have, you can find out by clicking here, filling in the account information, and clicking Submit Request. (No charge at that moment.)

You can find the person whose name is on the account, and their User Id, by looking at the very bottom of the Cloud screen, as shown below…

… or at the top of the Open / Save screen in the desktop software, as shown below.

Confirming the Edition You are Using

Cloud Edition subscribers may use either Cloud or desktop, so you may not know which edition you are using. To determine which edition you are using, look at the screen images below.

This is the desktop:

This is the Cloud:

Looking at these images will tell you which you are using.

If you are using the desktop, you will need to transition to the Cloud.

If other people in your office are using the desktop, they will need to transition to the Cloud.

Logging In to Cloud

If you have the Cloud Individual Edition, the person whose name is on the account may already log in to the Cloud.

If the person whose name is on the account is not currently logging in to the Cloud, all they have to do is to go to pro.flsgo.com and click “Forgot your password?”

That will allow them to reset their password. Then they can go to pro.flsgo.com and log in any time.

Transitioning to Cloud

If you are currently using the desktop software, then you will want to transition to using the Cloud.

Click here for help transitioning to using the Cloud.

Considering Cloud Firm

The Cloud Individual Edition licenses only one subscriber.

If there are more people in the firm who would like to access the software, you may wish to consider upgrading to the Cloud Firm edition.

The Cloud Firm edition includes the following benefits.

- Add all additional staff, each with their own logins, at no additional cost.

- Enable professionals and staff to view and edit each other’s files.

- Enable opening of files of professionals who have left the firm.

The Cloud Firm edition costs $10 more per professional per month than the Cloud Individual Edition. (Paralegals and non-financial staff of financial advisors are free.)

To upgrade to the Cloud Firm Edition:

- Click here.

- Enter the name, state, and User Id as shown above.

- Click Submit Request.

- Select Cloud Firm and continue.

As an alternative, you can have multiple Cloud Individual subscribers on the same account, but they will not be able to see each of these files and you will not be able to add staff.

If there is only one person in the firm, then stay with your Cloud Individual Edition. If more than one person wants to work in the software, however, then we really recommend Cloud Firm.

Add Additional Members

If you upgrade to Cloud Firm, you can add additional members through the Account Manager as follows:

- Log in to Family Law Software.

- In the upper right hand corner, click the Account button.

- Click the tile to Add/Remove Employees.

- Click the “+” button for each employee you wish to add.

Additional professionals will add $10 per month to your charge. Additional non-professional staff, such as paralegals, are free.

Add a System Administrator

When you add an employee, specify that they are a system administrator.

The person will then be able to log in themselves and add and remove employees.

If they do not get a registration email, they should do the following:

- Go to pro.flsgo.com.

- Click “Forgot your password?”

- Register.

- Go to pro.flsgo.com again.

They will be taken to the Account Manager.

Questions?

Click here for general questions about phasing out of the desktop software.

As you may know, Family Law Software is phasing out the desktop software on September 30, 2026.

This week will answer questions that Desktop Edition users may have about their next steps.

Confirming Your Edition

If you are not sure what edition you have, you can find out by clicking here, filling in the account information, and clicking Submit Request. (No charge at that moment.)

You can find the person whose name is on the account, and their User Id, by looking at the top of the Open / Save screen in the desktop software, as shown below.

You also see the User Id at the end of that line. You will want to know the User Id when you are upgrading the software.

Upgrading to Cloud

You will have to upgrade to one of the Cloud editions before September 30, 2026.

There are two cloud editions to consider, Cloud Individual and Cloud Firm.

If there are two or more people in the firm who would like to access the software, you may wish to consider upgrading to the Cloud Firm edition.

The Cloud Firm edition has the following benefits:

- Add all additional staff, each with their own logins, at no additional cost.

- Enable professionals and staff to view and edit each other’s files.

- Enable opening of files of professionals who have left the firm.

The Cloud Individual Edition costs the same as the desktop software you currently have. (If you pay annually, the software will reset your subscription to end a year from now and charge you the pro rated amount from the old renewal date to the new one.)

The Cloud Firm edition costs $10 more per professional per month than the Desktop software you currently have.

To upgrade to either Cloud Individual or Cloud Firm, do the following:

- Click here.

- Enter the name, state, and User Id as shown above.

- Click Submit Request.

- Select either Cloud Individual or Cloud Firm and continue.

As an alternative, you can have multiple Cloud Individual subscribers on the same account, but they will not be able to see each of these files and you will not be able to add staff.

If there is only one person in the firm, then Cloud Individual Edition is the way to go. If more than one person wants to work in the software, however, then we really recommend Cloud Firm.

Add Additional Members

If you upgrade to Cloud Firm, you can add additional members through the Account Manager as follows:

- Log in to Family Law Software.

- In the upper right hand corner, click the Account button.

- Click the tile to Add/Remove Employees.

- Click the “+” at the top to add employees

Additional professionals will add $10 per month to your charge. Additional non-professional staff, such as paralegals, are free.

Add a System Administrator

When you add an employee, specify that they are a system administrator.

The person will then be able to log in themselves and add and remove employees.

If they do not get a registration email, they should do the following:

- Go to pro.flsgo.com.

- Click “Forgot your password?”

- Register.

- Go to pro.flsgo.com again.

They will be taken to the Account Manager.

Transitioning to Cloud

Click here for general questions about phasing out of the desktop software.

If you have the Firm edition of the software, members of the firm may open the files of former members.

This includes former associates, ex-associates, partners who have left the firm, etc.

Here’s how:

In the File Manager, the person who wants to open the file should click “Case Files of Other Pro” (top right) and then check the box to include ex-associates. (That term is used generically and includes partners.)

The image below will illustrate:

The list will then include former associates and you may open their files to view and edit.

After we announced that we would be ending support for the desktop software, some of you have written to us with questions. Here are the questions we have received most often and our responses:

_________________________________________________________________________

Q: How can I know what edition I have?

A: Go to our Account Upgrade page. Fill in the information and submit. On the next page, you will see your current edition.

_________________________________________________________________________

Q: What does each edition cost?

A: You can learn about the prices and features of each edition on our pricing page. There is no one-time charge when you upgrade (that is, no $99 charge). If you have the desktop software, there is no additional charge to upgrade to the Cloud Individual edition.

_________________________________________________________________________

Q: How do I upgrade from the desktop edition at no cost?

A: Click here and choose the Cloud Individual Edition. For $10 more per professional per month, you can upgrade to the Cloud Firm edition. With the Cloud Firm edition, you can add unlimited staff at no additional cost, and members of the firm can view and edit each other’s files.

(If you pay annually, the software will reset your subscription to end a year from now and charge you the pro rated amount from the old renewal date to the new one.)

We recommend Cloud Firm if more than one professional in your office is using Family Law Software, or if you have multiple staff using the software. Cloud individual is a good choice if it is just you.

_________________________________________________________________________

Q: I have the Basic, Cloud or Firm edition (that is, not Desktop), but I have never logged in (or rarely). How can I get started using the Cloud software?

A: If you have a Cloud edition but have not been logging in to the Cloud, all you need to do to get started is go to pro.flsgo.com and click “Forgot your password?”

This FAQ will guide you through the rest.

_________________________________________________________________________

Q: If I upgrade now, can I continue using the desktop until September 30th?

A: Yes. But it would be best to gradually transition yourself to using the Cloud.

_________________________________________________________________________

Q: Do I have to manually upload my desktop files to the Cloud?

A: Yes. When you migrate to the cloud, decide which files you would like to work on currently and upload those files. Even after we terminate support for the desktop, you will be able to upload files that you created in the desktop software.

_________________________________________________________________________

Q: Can I do a bulk upload of files from my desktop to the Cloud?

A: Yes. Here’s how:

- Log in and click File Manager (top left).

- Click the Upload button (on the right).

- Select multiple files and click OK. (You can search on “how do I select multiple files in Windows Explorer.”)

_________________________________________________________________________

Q: What about my client data entry files?

A: Files that clients have worked on are already in the Cloud. You will see them when you first open the File Manager. If you upload the same file from your desktop, you will have two copies of the file. Choose one and archive the other.

To archive a file in the cloud:

- Open File Manager

- Find the line where the file is listed.

- Click the checkbox on the left on that line.

- Click the Archive button.

_________________________________________________________________________

Q: How can I find where my files are located on the desktop, to upload them to the Cloud?

A: It is shown at Files & Settings > Open/Save, as shown below.

_________________________________________________________________________

Q: What if I have different files in different locations?

A: You’ll have to upload from each location separately. One approach is to upload only the files you are currently working on. You can always upload any file you need later.

_________________________________________________________________________

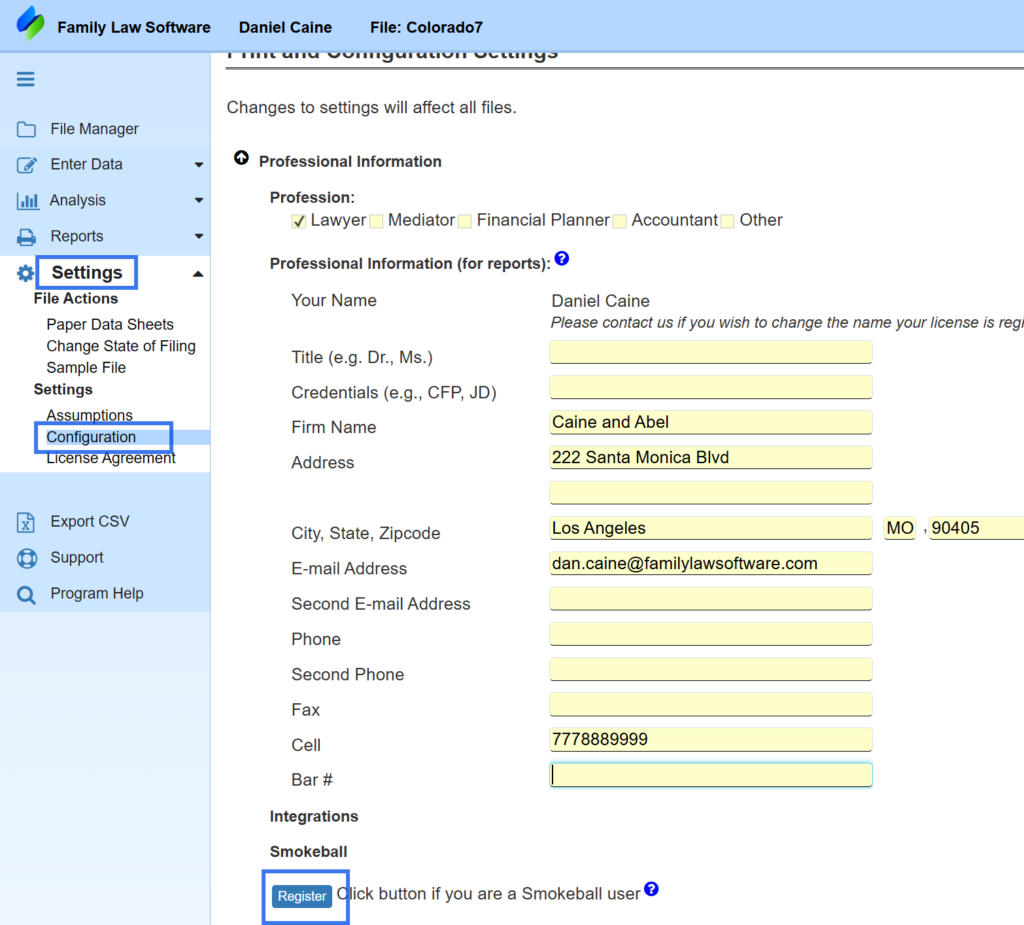

Q: I have Smokeball. What should I know?

A: Please see this FAQ for details.

_________________________________________________________________________

Q: Can I archive files in the Cloud?

A: In the File Manager, there is an option to archive files.

- Log in and click File Manager (top left).

- Click the checkboxes on the left of each file you wish to archive.

- Click the “Archive” button that will appear.

Also, you can set Auto-Archive timing in the File Manager, as shown below:

_________________________________________________________________________

Q: Do I have to upgrade to Cloud today?

A: No, you have until September 30, 2026. But the sooner you start, the more time you will have to smoothly transition. And please note that if your current edition is the desktop software, then the upgrade to Cloud Individual is at no additional cost. Click here to upgrade.

_________________________________________________________________________

Q: What if I never upgrade?

A: After September 30, 2026 you will not be able to update your software. After November 30, 2026, the software will no longer work. So you will want to upgrade at some point. Click here to upgrade now.

_________________________________________________________________________

Q: Can I use the Cloud software if I do not have a WiFi or other Internet connection?

A: You need a WiFi or other Internet connection to use the Cloud software.

_________________________________________________________________________

Q: What if I am on an airplane?

A: Most flights today offer WiFi, either free or for a charge. The WiFi is not always accessible, and it is sometimes slow. But in general you can work on Family Law Software cases while in flight.

_________________________________________________________________________

Q: What was that link again to the FAQ with instructions for transitioning to the Cloud?

A: It is here.

These questions will help people who are using Family Law Software and Smokeball together transition to the cloud.

Q: I have files that I am opening from within Smokeball on the desktop. How can I open them in the cloud?

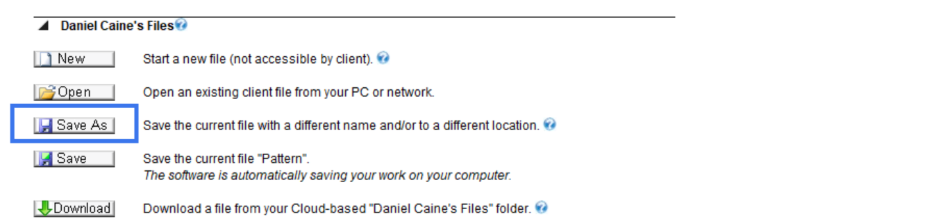

A: : The files that you open from within Smokeball are stored, each in its own somewhat hidden folder on your desktop. To find the location of the file, open the file and then click Files & Settings > Save As, as shown below.

That will show you the folder where that particular file is stored.

To upload that file:

Log in to the Cloud version

Open File Manager (top left)

Click the Upload button (on the right).

Navigate to that location on your desktop and click “OK.”

Our suggestion is that you upload files as you need them.

_________________________________________________________________________

Q: Can I open a Family Law Software Cloud file from within Smokeball for desktop?

A: No. You have to first upload the file as explained above.

_________________________________________________________________________

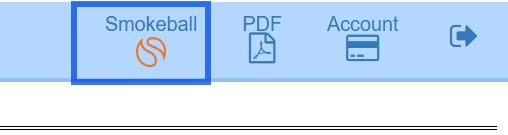

Q: Does the Cloud have a Smokeball integration?

A: Yes, you can upload PDFs to your Smokeball folder for the relevant matter. There is no ability to launch Family Law Software from within Smokeball for Cloud.

Please see this FAQ for details on the integration that exists.

_________________________________________________________________________

Q: I have the Basic Edition of Family Law Software Desktop. When I upgrade to the cloud, will I still be limited to the Basic Edition features?