448.22

Released July 22, 2026

For everyone

- File and case names. The file name can now be exactly the same as the case name.

- File upload. Files that are uploaded from the desktop will now all get the date the desktop file was last opened.

- Qualified Business Interest Deduction. The Qualified Business Interest Deduction (QBID) now calculates only for years the business is operating. It will not calculate, for example, after the owner retires.

State specific

Connecticut

- Support guidelines. We have released the update for the new child support guidelines for two-parent families. We are continuing to work on the new form for three-parent families.

Georgia

- The parenting adjustment is now correct when the first party is the father.

Illinois

- Child Support Guidelines. We have incorporated the option to use the new child support guidelines, which at this writing have not yet been fully enacted into law. If the start year is after 2026, shared parenting applies when both parties have 110 or more overnights, and presumptive minimum child support of $40 per child applies when the obligor’s income is 100% or less of the federal poverty guideline. These changes anticipate that SB 3524 will become law in August 2026, with an effective date of January 1, 2027.

Massachusetts

- Child Support Guidelines. We now calculate child support correctly when weekly income is in the range of $392 – $1000.

448.21

For everyone

- We changed the method used to restart the server, which should enable faster restarts when restarts are needed.

- We re-wrote the code in our tech stack, that communicates between the browser and the calculation code.

- We are hardening our security and we added code that allows us more closely to track any potential security breaches.

State specific

California

- Child Support Data Entry. We removed the “Disso Style” child support data entry sub-tab and renamed “FLS Style” to simply “Data.”

- Navigation. We fixed navigation back to the Support screen after changing the tax year. (This was an issue only in the Cloud edition.)

- Support Worksheet. The California Child Support Worksheet now shows the correct amount for Spousal Support even if the actual exemptions are not tax-optimized.

- Self-employment income. The self-employment income field under “Other Income” on the Child Support Data screen is now included on FL-150 line 7.

- Judicial Council forms. We released an updated FL-311.

448.20

For everyone

1. Health insurance. We have taken another pass at the health insurance tax categories to try to make them clear. The tax categories for health insurance now are:

- Pre-tax. This means the health insurance reduces taxable wages for both income tax and FICA purposes. This will apply to a majority of today’s employer-provided health insurance and we select this category by default.

- Pre-tax, FICA-taxable. This means that the health insurance reduces taxable wages for income tax purposes but not for FICA purposes.

- Self-employed. These are health insurance premiums paid by a self-employed individual, or partnership. They are subtracted from income “above the line” for federal income tax purposes, and also for self-employment tax purposes.

- After-tax. These are out-of-pocket payments of health, dental, and vision premiums that are not payroll deductions. These are treated as medical expenses, subject to the 7.5% AGI threshold. This means that they are not deductible for most individuals, either because the taxpayer uses the standard deduction and does not itemize, or because their medical expenses are less than 7.5% of their Adjusted Gross Income, or both.

2. Minimum wage. We updated the minimum wage rates that have changed since our last update. Those include rates in Alaska, D.C., and Oregon.

State specific

California

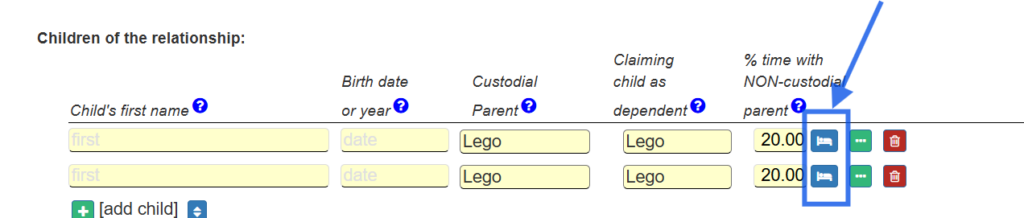

- Self-employment income. Entries in the new self-employment income field are now included in guideline income.

- Wages. You can now specify that wages are self-employment income in the FLS Style screen using the “show more” option.

- Overnights calculator. We have now restored the overnight calculator that we inadvertently removed. You can find this calculator on the line where you enter information about each child, as shown below.

Florida

- Arrears. We have updated the child support arrears rate to the 7/2026 rate.

New Jersey

- Appendix IX-E. We updated Appendix IX-E to the new June, 2026 rules.

- Appendix IX-H. We updated Appendix IX-H to the new June, 2026 rules.

- Child Care. We fixed a rounding issue on line 8 of New Jersey Child Care Cost Worksheet.

448.19

For everyone

- Notifications. We now have the ability to send in-app notifications on either a general or state-specific basis.We will use this to keep you updated with regard to significant updates, fixes, and enhancements in the software.

- Budget Report. If you were viewing one party only, on a weekly, monthly, annual basis, then the spousal support was not appearing. This is fixed.

State specific

California

- Child Support What If. Now, instead of overnights, we show % time for the non-custodial parent. We also now show the amount of support paid for other children to enable multi-family scenarios.

- Judicial Council Forms. Updated FW-001, FL-335 and FL-341(A).

Florida

- Alimony. On the Quick child support screen, we now ask for the alimony end date. This enables a more accurate Child Support stepdown calculation.

New York

- Child support. The health insurance income limitation now applies only if the SCHIP/MA calculation is used.

448.18

For everyone

- Health Insurance tax categories. We have updated the pre-tax labels on the health insurance tax category drop-down to be more clear. They now read “Pre-tax & FICA-exempt” and “Pre-tax & FICA taxable.”

- Marital Property Division. We now show the unallocated amount even if it is negative. There could be a negative unallocated amount if debts exceed assets.

- RSU. If you enter restricted stock units on the RSU table, that will overwrite any value you previously entered for the asset. We now make that more clear.

- Required minimum distributions. We have now updated the default start date for required minimum distributions from IRA and 401(k) plans to be age 73.

- Arrears. We have updated the state-specific arrears interest rates.

- “Net income” label on Budget Report. The net income label now appears fully when the user has entered one or more discretionary expenses.

- “Tips” deduction. We now explain the new tips deduction, where tips are entered.

State-specific changes

California

- Improved Child Support Data Entry Screen consolidates quick and complete in a single screen.

- Updated the following California PDF forms:

- FL-305

- FL-300-INFO

- RI-FL024

- RI-FL035

- CLETS-001

- FL-324(P)

- FL-324(NP)

- Improvements to FL-105, FL-700, FL-710, and FL-720

Colorado

- Users of the Quick tab on the Child Support data entry screen, and of the Personal Edition, can now specify to use the prior guideline or the current guideline.

Florida

- High incomes. We now explain how we calculate child support for combined incomes over $10,000.

Illinois

- Affidavit. We now reset the county on the Affidavit and guideline worksheets if it is changed on the Affidavit data entry screen.

Massachusetts

- PDF – update TC002

- Child support. We now exclude prior relationship child support from income for the child support calculation

New York

- Maintenance. The maintenance amount at the top of the screen will appear only if it is currently being calculated.

448.17

No visible changes.